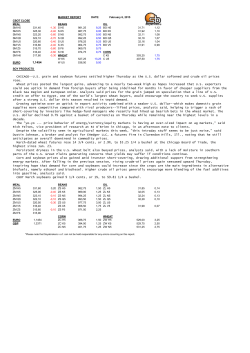

MARKET SNAPSHOT Build in on th g stro e n toep g fer herit age 5 DECEMBER 2014 The trading week Market Last Trade 7 Day Move CBOT Wheat ($USc/bu) 589.75 27.75 CBOT Corn ($USc/bu) 389.75 11.5 CBOT Beans ($USc/bu) 1010.5 36.5 Winnipeg Canola ($CAN/Mt) 412.7 14.4 Matif Canola (€/ Mt) 336.75 1 AU$ / US$ 0.8385 0.0156 AU$ / EUR 0.6772 0.0184 WHEAT GLOBAL Impressive gains create more bullish mood Global wheat values have staged impressive gains over the past month, with front month CBOT wheat testing key resistance levels to the upside. Despite this, US wheat does not currently price to most importing destinations when compared with other origins. However, CBOT wheat derivatives remain an important product for the global Index and alpha funds, which consider CBOT a global benchmark for pricing, offering transparency and liquidity, albeit they do add to volatility. Today, the AT A GLANCE ADM PORT PRICES APW1 (15/16) APW 1 GA1 Malt F1 Non GM Canola Sorghum 293 Brisbane 302 325 300 Newcastle 302 306 285 463 298 Pt Kembla 302 303 275 461 Geelong 302 303 310 275 466 Pt* Prices Adelaide are indicative 292 278 320 260 455 Kwinana (Port inc) 307 308 320 285 483 and subject to change * Prices are indicative and subject to change. speculative fund position in wheat is approximately square. DOMESTIC Macro themes remain at the forefront, with monetary easing measures for the EU and China all underpinning the US Dollar, but contributing to the bearish tone of the AUD, Euro and Yen, while the Russian Rouble collapsed. Australian east coast wheat remains a domestic affair, with current pricing in the BNE zone $40USD above export parity, while Port Kembla and VIC remain at approximately $17-20USD over. North-eastern Australia is waiting for a decent summer rain, which will help summer crops and aid continued plantings. Summer crop conditions will be the driver for pricing going forward of wheat Earlier this week, CBOT March wheat had closed above 600c/bu, testing the 180-day moving average. In late September, we had march CBOT wheat testing 480c/bu to the downside, from where prices have ground higher, culminating in a post-Thanks Giving Day rally putting on 45c/bu in a few trading sessions. Winter wheat issues have contributed to the bullish tone, with concerns over possible winter kill namely in Russia, Ukraine and the US. A lot of discussion on whether there has been enough early snow cover to protect against cold conditions continues to circulate. It was also rumoured that the Russian Government was looking to entertain a tariff on future wheat exports, however, it appears it remains rumour only. Basis values soften in north-eastern Australia. WA and SA wheat values are currently $12-15USD away from working into the Middle Eastern destinations on nominal grades, while at current values we are pricing into Asia. Despite this, Australian wheat basis values have softened in recent weeks. In WA we have seen values weaken in basis terms from 140c/bu to 100c/bu over December CBOT wheat, while SA values have traded from 135c/bu down to 60c/bu. MARKET SNAPSHOT PAGE 2 BARLEY Firm trend continues Generally speaking, the barley market (for both feed and malt) has been a stronger performer since the commencement of harvest. Other than the Victorian Mallee and Wimmera, quality has been very good and yield reports from growers suggest the crop has fared well despite the dry finish. The market has remained firm during harvest and maintained itself with the retreating Aussie dollar. Short covering from both domestic and export buyers, in CANOLA addition to demand from China, is definitely sustaining current malt spreads and price levels, all while growers remain active sellers. From an export demand perspective, the market is looking to cover April to July requirements via both bulk and containers. On the domestic front, we would expect local buyers to remain consistent with their nearby purchases in the hope the market may settle once the peak shipping period passes. Negative crush margins weigh on demand Canola futures have continued to take the lead from soybeans over the last month, which has ultimately been driven by nearby demand for meal. Slow grower selling and the delayed US bean harvest kept processing pipelines tight which, in turn, has followed onto futures markets. The US bean harvest is currently 99% finished following some delays due to wet weather. Nearby soy crush margins continue to be solid, which has allowed crush capacity to remain strong. This throughput should alleviate the meal shortage in a relatively short period. Matif futures have too been supported by positive nearby crush margins, although, at current levels, these drop away into the new year. Capacity is being switched to soybeans where possible and demand for rapeseed will be reduced into the new year. Negative canola crush margins in China have also weighed on demand for canola seed, with Chinese buyers currently showing little interest at current levels. As with European crushers, Chinese crushers have switched to soybeans where possible due to better margins. All this appears to equate to lower volumes of canola heading to China in the coming year. Aussie seed continues to be expensive compared with Canadian seed and, at current levels, will struggle to see much additional demand basis Canadian. MARKET SNAPSHOT PAGE 3 CANOLA continued Canadian logistics appear to be tracking okay, with Canadian government officials announcing on Saturday that minimum grain volume shipment requirements for railways will be extended to March, which should reduce the risk of logistical bottlenecks that were experienced last year. ABARE has lowered 2014/15 Australian canola production to 3.32 mln t from September’s estimate of 3.39 mln t. The canola harvest is complete in many areas, with most only experiencing minor weather delays. The falling Australian dollar has helped support Aussie prices in the short term and growers appear happy to sell some tonnes now that the canola harvest is relatively complete. The global canola / rapeseed complex S&D continues to be relatively relaxed considering reasonable production and reduced demand. MAKING NEWS... ADM loads largest ever Australian canola shipment Archer Daniels Midland Company’s The vessel will then dispatch at ADM’s dry-bulk vessels that will be delivered (NYSE: ADM) newest oceangoing vessel, Europoort facility in Rotterdam, to ADM by Oshima Shipbuilding Co in the MV Harvest Frost, recently sailed its Netherlands, on around December 24, the next few months, bringing ADM’s maiden voyage out of Australia loaded where the product will be crushed and with the largest export shipment distributed throughout Europe. oceangoing vessel count to 11. Loading of the MV Harvest Frost at CBH’s of canola in the nation’s history – The Harvest Frost is the first of three new Kwinana facility in Western Australia. 77,612.20 metric tonnes. 95,000MT (dead weight) post-Panamax Photo: NJ Humphrey Photography. MARKET SNAPSHOT PAGE 4 SORGHUM Precipitation Forecasts Precipitation (mm) during the period: Wed 03 Dec 2014 at 12Z to Thu 11 Dec 2014 at 12Z Thu 11 Dec 2014 at 12Z to Fri 10 Dec 2014 at 12Z Precipitation (% of normal) during the first period: Wed 03 Dec 2014 at 12Z to Thu 11 Dec 2014 at 12Z Rain dances continue Everyone continues to wait for rain. Hot and dry weather has been the story of the past two months, when growers have been crying out for moisture to fill the severely depleted soil profiles. 250 200 175 150 125 100 90 80 70 60 50 40 35 30 25 20 16 13 10 7.5 5 2.5 2 1.5 1 0.5 There have been some showers across southern Queensland the past month, but not the 75mm+ that is needed for a widespread plant. Showers are forecast this weekend that look very encouraging, but again, it will only prove to be worthwhile once it’s in the rain gauge. There has been many a false forecast over the past six months. The crop that is in the ground is 800 600 400 300 150 75 50 25 10 5 Central Queensland & Southern New South Wales Michael Vaughan | 0427 308 317 starting to suffer from the lack of moisture (see crop photo that is representative of the current crop in northern NSW). If the rain does eventuate, it will be too late to significantly improve these crops, but it will provide a good base for the subsequent plant. We just need the rain!! In other news, Argentina and China have signed an agreement to allow Argentinean origin sorghum to be imported into China. The details of the agreement are still a bit hazy and it may take some time to analyse the possible impact on the market. Victoria Peter Sidley | 0427 517 417 [email protected] Western Australia Reece Duffield | 0418 589 334 [email protected] [email protected] Precipitation forecasts from the National Centres for Environmental Prediction. Normal rainfall derived from Xie-Arkin (CMAP) Monthly Climatology for 1979-2003. Forecast initialisation time: 12Z0CDEC2014 South Australia Southern Queensland & Northern New South Wales Peter Dorney | 0428 214 986 [email protected] Ben Noll | 0407 180 526 [email protected] www.admgrain.com.au Connecting the harvest to the home

© Copyright 2026 ExpyDoc