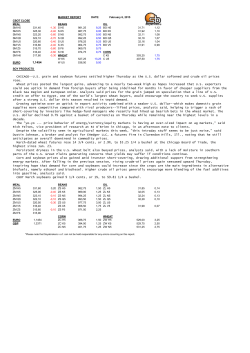

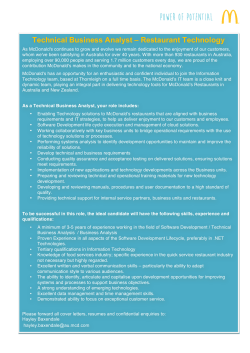

Equity Research FIBRA UNO FIBRA / Diversified March 05, 2015 Utah’s Portfolio Acquisition Is Completed Buy Buy Reiterated FUNO11 Liquidity: Change in Recommendation High Last Price: MX$ 42.08 Price Target 2015: MX$ 60.00 Change in T.P. Change in Estimates Dividend Yield 2015: 42.6% E. Return Quarterly Review Other FUNO announced today it has closed Utah’s portfolio acquisition for USD67.9 million. This portfolio includes a Class A+/A office building with 16,348 sqm of gross leasable area (GLA), located in a premium location in the Reforma-Lomas corridor (in the corner of Montes Urales and Volcan streets), in Mexico City. Bancomer is the property’s tenant, with most of its leasing contracts being triple net (higher profitability for FUNO), denominated in US dollars. It is worth to mention that this acquisition was already announced by the trust. Another Accretive Acquisition. The property was acquired with a 100% occupancy and it is expected to generate USD6.0 million of annual net operating income (NOI), representing a gross entry NOI cap rate of 8.8%, or 8.3% net NOI to the FIBRA (accounting for the F1, F2 and acquisition fees). The net EBITDA cap rate to FUNO is 7.8% (after the F3 advisory fee), which implies a 320bps spread against FUNO’s current forward adjusted cap rate. The transaction was paid 100% with cash and the property has no debt. 6.4% Total Return: 49.0% Stock performance 115 110 Return Index Local Ticker: 105 100 95 90 85 Dec-13 Apr-14 Jul-14 Oct-14 FUNO11 Jan-15 IPC Market Data: This announcement is marginally positive for FUNO as we were expecting it to be closed during 2Q2015. According to FUNO, it takes on average 4 months to close acquisitions due to their pertaining processes and the corresponding approval from the Mexican antu-trust authority (COFECE). The Utah portfolio was disclosed during FUNO’s investor day held in NYC on October 28, 2014, however its purchase agreement was signed on January 20, 2015. Buy Reiterated. At current MX$42.00 price levels FUNO presents a new entry opportunity on its more attractive valuation amidst a year of consolidation of its aggressive investment cycle, in our view. Our Buy recommendation is reiterated. We will soon release a company update note. Market Cap (MX$ MM): 125,352 Firm Value (MX$ MM): 141,243 LTM Price Range (MX$): (38.44 - 47.86) Free Float: Avg. Daily Trade (MX$ MM): Utah Portfolio (Bancomer Office Building) Source: Google Earth, FUNO, Actinver. Pablo E. Duarte de León Real Estate [email protected] +52 (55) 1103 6600 x4334 Actinver Guillermo Gonzalez Camarena 1200 Santa Fe, Mexico City, 01210 Actinver’s Equity Research 82% 327.8 Equity, Economic, Quantitative and Fixed Income Research Departments Equity Research Gustavo Terán Durazo, CFA Senior Analysts Head of EquityResearch (52) 55 1103-6600 x1193 [email protected] Martín Lara Telecommunications, Media and Financials (52) 55 1103-6600x1840 [email protected] Carlos Hermosillo Bernal Consumption (52) 55 1103-6600 x4134 [email protected] Pablo Duarte de León FIBRAs (REITs) (52) 55 1103-6600 x4334 [email protected] Pablo Abraham Peregrina Mining, Metals, Paper and Conglomerates (52) 55 1103-6600x1395 [email protected] Ramón Ortiz Reyes Cement, Construction and Concessions (52) 55 1103-6600 x1835 [email protected] Federico Robinson Bours Carrillo Energy, Chemicals and Industrial (52) 55 1103-6600 x4127 [email protected] Juan Ponce Telecommunications, Media and Financials (52) 55 1103-6600x1693 jponce@actinver,com.mx Enrique Octavio Camargo Delgado Energy, Chemicals and Industrial (52) 55 1103-6600x1836 [email protected] José Antonio Cebeira González Consumption (52) 55 1103-6600x1394 [email protected] Mauricio Arellano Sampson Mining, Metals, Paper Conglomerates , Cement, Construction and Concessions (52) 55 1103-6600 x1835 [email protected] Junior Analysts Economic and Quantitative Research Ismael Capistrán Bolio Head of Economic and Quantitative Research Jaime Ascencio Aguirre Economy and Markets Santiago Hernández Morales Quantitative Research Roberto Ramírez Ramírez Quantitative Research Roberto Galván González Technical Research (52) 55 1103-6600 x6636 (52) 55 1103-6600 x1100 (52) 55 1103-6600 x4133 (52) 55 1103-6600x1672 (52) 55 1103 -66000 x5039 [email protected] [email protected] [email protected] [email protected] [email protected] Fixed Income Research Araceli Espinosa Elguea Head of Fixed Income Research (52) 55 1103 -66000 x6641 [email protected] Jesús Viveros Hernández Fixed Income Research (52) 55 1103 -66000 x6649 [email protected] 2 Disclaimer Guide for recommendations on investment in the companies under coverage included or not, in the Mexican Stock Exchange main Price Index (IPC) • StrongBuywith an extraordinary perspective. According to the analyst, in the next twelve months, the valuations of stock and/or prospects for the sector are EXTREMELY FAVORABLE • Buy. According to the analyst, in the next twelve months, the stock’s valuation and / or prospects for the sector are VERY FAVORABLE • Neutral. According to the analyst, in the next twelve months, the valuation of stock and / or sector ARE NEUTRAL OR FAVORABLE but with a similar perspective to the IPC • Belowmarket. According to the analyst, in the next twelve months, the valuation of stock and / or sector outlook ARE NOT POSITIVE • Sell. According to the analyst, in the next twelve months, the valuation of stock and / or sector outlook ARE NEGATIVE, or likely to worsen • In reviewwith positive outlook • In review with negative or unfavorable perspective ImportantStatements. a) Of theAnalysts: “The analysts in charge of producing the Analysis Reports: Jaime Ascencio Aguirre; Mauricio Arellano Sampson; Enrique Octavio Camargo Delgado; Ismael Capistrán Bolio; José Antonio Cebeira González, Pablo Enrique Duarte de León; Araceli Espinosa Elguea; Roberto Galván González; Ana Cecilia González Rodríguez; Carlos Hermosillo Bernal; Santiago Hernández Morales; Martín Roberto Lara Poo; Ramón Ortiz Reyes; Pablo Abraham Peregrina; Juan Enrique Ponce Luiña; Federico Robinson Bours Carrillo; Gustavo Adolfo Terán Durazo; Jesús Viveros Hernández, declare”: b) 1. "All points of view about the issuers under coverage correspond exclusively to the responsible analyst and authentically reflect his vision. All recommendations made by analysts are prepared independently of any institution, including the institution where the services are provided or companies belonging to the same financial or business group. The compensation scheme is not based or related, directly or indirectly, with any specific recommendation and the remunerationis only received from the entity which the analysts provide their services. 2. "None of the analysts with coverage of the issuers mentioned in this report holds any office, position or commission at issuers underhis coverage, or any of the people who are part of the Business Group or consortium to which they belong. They have neither held any position during the twelve months prior to the preparation of this report. " 3. "Recommendations on issuers, made by the analyst who covers them, are based on public information and there is no guarantee of their assertiveness regarding the performance that is actually observed in the values object of the recommendation" 4. "Analysts maintain investments subject to their analysis reports on the following issuers: AC, ALFA, ALPEK, ALSEA, AMX,AZTECA, CEMEX, CHDRAUI, FEMSA, FIBRAMQ, FINDEP, FUNO, GENTERA, GFREGIO, GRUMA, ICA, IENOVA, KOF, LAB, LIVEPOL, MEXCHEM, OHLMEX,POCHTEC, TLEVISA,SORIANA, SPORTS, VESTA, WALMEX. On Actinver Casa de Bolsa, S.A. de C.V. Grupo Financiero Actinver 1. Actinver Casa de Bolsa, S.A. de C.V. GrupoFinanciero Actinver, under any circumstance shall ensure the sense of the recommendations contained in the reports of analysis to ensure future business relationship. 2. All Actinver Casa de Bolsa, SA de C.V. GrupoFinanciero Actinver business units can explore and do business with any company mentioned in documents of analysis. All compensation for services given in the past or in the future, received by Actinver Casa de Bolsa, SA de C.V. GrupoFinanciero Actinver by any company mentioned in this report has not had and will not have any effect on the compensation paid to the analysts. However, just like any other employee of Actinver Group and its subsidiaries, the compensation being enjoyed by our analysts will be affected by the profitability gained by Actinver Group and its subsidiaries. 3. At the end of each of the previous three months, Actinver Casa de Bolsa, SA de C.V. Actinver Financial Group, has not held any investments directly or indirectly in securities or financial derivatives, whose underlying are Securities subject of the analysis reports, representing one percent or more of its portfolio of securities, investment portfolio, outstanding of the Securities or the underlying value of the question, except for the following: * AEROMEX, BOLSA A, FINN 13, FSHOP 13, SMARTRC14. 4. Certain directors and officers of Actinver Casa de Bolsa, SA de C.V. GrupoFinanciero Actinver occupy a similar position at the following issuers: AEROMEX, MASECA, AZTECA, ALSEA, FINN, MAXCOM, SPORTS, FSHOP and FUNO. This report will be distributed to all persons who meet the profile to acquire the type of values that is recommended in its content. To see our analysts change of recommendations click here. 3

© Copyright 2026 ExpyDoc