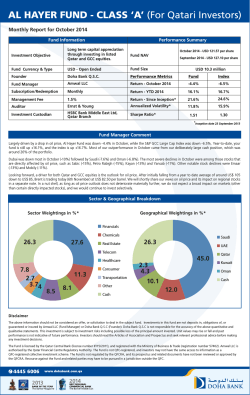

THE GCC – OPPORTUNITIES IN HEALTH FUNDING AND MEDICAL TOURISM 6th Arab German Health Forum 2013 2 Demographic Changes and Future Population Trends GCC Population has grown considerably over the past 5 years 3 Population, GCC (2008-2013) Population (Million) 42.0 • The GCC population expanded at CAGR of 2.2% to 41.6 million during 2008-2013. • The expatriates make up to 49% of the region’s population. • UAE has the highest expatriate population and Saudi Arabia has the lowest. 40.0 40.0 39.1 39.0 38.0 40.8 CAGR:2.2% 41.0 41.6 38.2 37.4 37.0 36.0 35.0 2008 2009 2010 Source: International Database- Census bureau 120% 2011 2012 2013 Years Percentage of National and Expatriates, GCC,2009 Population 100% 62% 51% 75% 60% Nationals 75% Expatriates 40% 38% 75% 70% 61% 20% 25% 30% 39% 80% 49% 25% 25% 0% Bahrain Kuwait Source: Frost & Sullivan 2012,report Oman Qatar Saudi Arabia Countries UAE GCC GCC Population is expected to rise to over 50 mn in 2025 4 Population Projections,GCC,2010-2025 Population (millions) 60.0 50.0 40.0 39.1 45.4 43.2 41.6 46.9 50.2 • By 2025, the population in GCC will reach 50 million. The vast majority will be under the age of 25. • Growth in GCC is largely due to increasing number of expatriates in the region’s developing economies. • GCC is expected to be a major importer of foreign labor in future as well. 30.0 20.0 10.0 0.0 2010 2013 2015 2018 2020 2025 Years Source: International Database-Census bureau Population Projections by Country,GCC,2010,2015 and 2025 Population(million) 2010 35.0 30.0 25.0 20.0 15.0 10.0 5.0 0.0 2015 2025 31.9 27.8 25.7 1.2 1.3 1.6 Bahrain 2.5 2.8 3.2 3.0 3.3 4.0 1.7 2.2 2.6 Kuwait Oman Qatar Source: International Database- Census bureau Country 7.1 5.0 5.8 Saudi Arabia United Arab Emirates Overall population is set to rise, the +65 population is set to grow significantly 5 Population Projection, GCC (2010-2050) 70.00 Population (millions) 60.00 50.00 40.00 43.1 46.9 50.2 53.1 55.1 58.0 60.1 61.9 12.9 65+ age mn 46.5 mn 39.1 65+ 15-64 age 30.00 15-64 0-14 20.00 11.1 mn 10.00 0-14 age 0.00 2010 2015 2020 Source: International Database- Census bureau 2025 2030 2035 2040 2045 2050 Years • Population growth in GCC is heavily driven by immigration trends in the region. • In addition, improvement in life expectancy over past quarter of a century have lead to the expansion of over 65 age group segment. • The elderly population in the region is expected to grow leading to increase demand in healthcare in future 6 Health Indicators, Spending and Risk Factors in the GCC – A snapshot GCC – Health Indicators and Risk Factors NCD’s a % of total for cause of mortality 66% 83% 71% 69% 76% 79% 69% 72% 79% 71% 33% 33% 42% 33% 33% 34% 29% 37% % Overweight out of total population 71% 56% % Obesity out of total population 33% 21% % at risk from raised blood pressure 28% 35% WHO: Non communicable diseases country profiles 2011 Overweight Prevalence – A global snapshot 8 GCC – ranges from 51-60% to over 71% Rising Prevalence of Diabetes in the GCC, a leading risk factor for CVD 9 Comparative Prevalence of Diabetes (2011, MENA Region) Projected burden of cardiology – 2006 vs 2025 (est.) 44% Others Cardiovascular disease 12% Infectious diseases 11% 12% Maternal and perinatal conditions Source: IDF 2011 7% 8% Genitourinary diseases 6% 7% 0% 2025 ▪ 5 of the 6 GCC countries in the top 10 countries in the world in terms of % prevalence of Diabetes (2011 Diabetes Atlas). ▪ Lifestyle disease such as diabetes, Hypertension, Heart diseases accounts to 50% of deaths in Gulf region. Source: McKinsey & Co. Research 24% 7% 10% Digestive diseases ▪ Diabetes prevalence is over 25% of the GCC population. 52% 20% 2006 40% 60% Per Capita Total Expenditure on Health in the region is reasonable but lower than OECD Avg. However, the healthcare spending is significantly higher than rest of Middle East where the current spending is grossly inadequate to meet healthcare demand in a number of the countries Source: Global Health Expenditure Database, WHO 2012 and OECD Health Data 2012 A large portion of the health spending in the GCC is financed by the Government Efforts are being made by many Gulf States to shift the burden of spending from the Government and OOP to health insurance Source: Global Health Expenditure Database, WHO 2012 and OECD Health Data 2012 There has been an Increase in spending on Healthcare(per capita) since 2005 12 Health expenditure($) 1400 Average per capita expenditure on Health,GCC, 2005-2010 • During 2005-2010,per capita health spending in GCC has grown in tandem with rise in income. CAGR:8.7%(2005-2010) 1200 1000 800 600 400 200 0 2005 2006 2007 Source: World bank 2008 2009 • The growth is quite significant in UAE compared to other GCC countries. 2010 Years Per capita expenditure($) Per capita Health expenditure by Country, GCC 2,500 2,000 1,500 1,000 2005 500 2010 0 Oman Saudi Arabia Bahrain Country Source: World bank, IDB-census bureau Kuwait Qatar United Arab Emirates Health Spending in the GCC – Future trends • The healthcare services market in GCC expanded at a CAGR of 18.8% since 2004 and reached around USD23.1 billion in 2009. • It is projected to grow at an annual rate of 11.4% to USD43.9 billion by 2015 from an estimated USD25.6 billion in 2010 • Some experts estimate spending to grow to USD 60 billion in 2025 with growth in inpatient and outpatient market due to increased disease prevalence coupled with rising healthcare cost/inflation 13 Source: Alpen Capital GCC Healthcare Report 2011, Mc Kinsey & Co. GCC Healthcare Outlook Health Market Growth in the GCC Saudi Arabia and the UAE are the largest markets together accounting for 75% of health spending in 2015 and are expected to be the fastest growing markets in GCC over 2010–15 growing at over 12% Country-wise healthcare market within GCC (%) Source: Alpen Capital GCC Healthcare Report 2011 14 Country-wise healthcare market growth over 2010-15 15 Overview of Future Health Investments in the GCC Upcoming Healthcare Projects in GCC 16 Some of Country the major is not an exhaustive Project projects in the region (this Status Value list) Kuwait Jaber Al Ahmed Al Sabah hospital Construction $1057 m Razi Hospital Construction $ 1200 m Sidra Medical & research Design $ 2300 m Oman Medical City Oman Concept Stage $1000m Saudi Arabia 10 Specialized hospitals in Saudi Arabia Concept Stage $1,350m Prince Nayef Specialization Medical city Concept Stage $1,000m King Abdullah Medical City Design $1,200m New Hospital for Sheikh Khalifa Medical City Design $2,000m Cleveland Clinic in Al Maryah Island Construction $1,300m UAE Source : Frost& Sullivan Report 2012, Alpen GCC Healthcare Report 2011, Contructionweekonline.com Upcoming Healthcare Projects in Dubai 17 Project No. of Beds Public Al Jalila Pediatric Hospital 200 Al Makhtoum Trauma Hospital 400 Private University Hospital (DHCC) Al Jord Orthopedic Specialty Hospital 400 53 Suliman Al Habib Hospital expansion 200 Aster(DM Healthcare) Dubai 300 The City Hospital expansion (Oncology) 200 Lifeline – Umm Hurrair Hospital 94 Al Zahra Hospital 200 Source : Dubai Health Authority/ DHCC 18 Financial Challenges in the GCC Health System Financial challenges facing the region Increase “pre-payments” through health insurance, levies and/ or taxes Reduce government burden on health expenditure Reduce Out-of-Pocket expenditure by increasing health insurance coverage Complexity projecting future health spending, which requires; Current expenditure on hospitalization, doctor visits, pharma. Demographic factors: population structure Health factors: burden of diseases Economic and social factors: income, new technologies Public policy factors: health promotion, health regulation Health Insurance can play a role in promoting investments & reducing the prevalence of lifestyle diseases Insurance industry can design and implement innovative health coverage packages that have varied benefits and have a specific focus on prevention Benefits of future Health Insurance packages Primary prevention –They include immunization, smoking cessation, regular physical activity, good nutrition etc. Secondary prevention - It includes Pap smears, blood pressure check-ups, mammograms, and other forms of screening. Tertiary prevention - Tertiary prevention may include both drug treatments and actions like physical activity and good nutrition that can help control heart disease and hypertension. GCC Employers are likely to adopt health insurance schemes that are aimed at reducing cost. Specific Programs focusing on wellness & prevention could be an innovative approach e.g Weight loss or smoking cessation. Booz & Co’s GCC’s Insurance Mandate Medical Tourism – Overview and Opportunities Industry Drivers: Factors that have lead to the rise of Medical tourism Government policy - Around 50 countries have now identified medical tourism as a strategic national industry. In Asia, one impetus came from the Asian crisis of 1997, when some countries seized on medical tourism as a way to increase foreign currency earnings. Developments in information technology - The Internet has enabled patients to research options beyond national borders, and has expanded international marketing opportunities. It has also broken down cultural barriers. Lower air fares -The advent of budget airlines and a drop in airline fares have made foreign travel-and therefore medical tourismmore affordable. Trade liberalization - The General Agreement on Trade in Services, agreed by the World Trade Organization (WTO) in 1996, paved the way for trade in medical and other services. Increasing foreign investment - The relaxation of restrictions on foreign ownership in many emerging-market economies has channeled FDI into provision of healthcare services, leading to improvements in quality and efficiency. Internationalization of the medical workforce - As healthcare systems have expanded, developed countries have recruited more immigrant healthcare workers. This has given medical staff valuable international experience, and has allowed Western patients to become familiar with dealing with foreign medical staff. Internationalization of medical training and accreditation - The vast majority of IMGs in the US trained in developing countries, which originally led to concern over standards. This prompted some harmonization of medical training, which, combined with the spread of English as an international language, has made medical skills more portable. The rise of facilitator firms - Thousands of agencies now offer medical tourism services to healthcare travelers, such as arranging accommodation and acting as a mediator with the hospitals. These agencies also act as a channel for governments and hospitals to promote medical services. Source: Healthcare Special report - EIU 2011) Drivers demand for Outbound Medical Tourism from GCC Medical tourism provides an opportunity to reduce costs for blue collared workers and those without insurance coverage. People with health insurance opting to travel abroad for quality or value as they pay out of pocket for elective surgery and “pre-existing conditions” Very often, patients tend to travel for better quality of care which can be offered in a more mature and evolved health system such as Germany, France, UK Patients travelling to centers of excellence for critical care. Singapore and Germany attract a lot of Gulf patients for Oncology Drivers of demand for outbound tourism Growing incidence of lifestyle diseases like CVD, Cancer, Diabetes is encouraging health and wellness procedures abroad Lack of availability of certain health and wellness treatments encourage the outbound travel for e.g. fertility, sports medicine, cosmetics The reasons behind a decision to travel for healthcare The factors that could affect each patient’s choice of location are: Expertise of the doctors or surgeons involved, and the quality of aftercare; Ease of travel, including the possibility of combining treatment with a holiday; Familiarity with the country, the language and the healthcare system; Risks for the patient, which range from quality concerns in the healthcare system to general risks, such as terrorism; Cost, both for the treatment and for the stay. The perceived value from treatment abroad considering the quality of health system in the home country and malpractice by clinicians. The waiting time for the procedure in the home country compared with the location they consider for medical travel. The availability of after care services post surgery The availability of information on quality and experience of surgeons and on the costs Source: Healthcare Special report - EIU 2011 and DHA Overseas Treatment Survey 2012 Perceptual Mapping of leading destinations in Medical Tourism Developing a brand on the strength of its tourism and hospitality sector. Focus on elective procedures Costa Rica is very successful with US patients seeking elective procedures. India for cardiac and orthopedic globally Jordan Korea Canada Singapore US Switzerland UK Germany France Belgium Dubai Greece Malaysia Turkey Spain Thailand Costa Rica India Poland Tourism Focus Bulgaria Romania South Africa Hungary Czech Rep. Value Focus Hungary and Czech Republic – growing popular, good quality care with 30-50% cheaper prices than UK, Germany for cosmetic, dental, fertility, spas. Tourists from Austria, Germany, Russia, UK A well developed medical tourism offering focusing on certain specialties and treatments. Although expensive, Germany is respected for high quality care and its technological edge and innovation in clinical services Clinical Quality Focus All destinations for medical tourism are positioned to compete based on either the clinical quality and the strength of their health system or on the strength of their tourism brand and infrastructure Factors limiting the growth of outbound medical tourism in the GCC Considerable investments in public and private sectors are being made to expand services and keep patients at home. Bad experiences and poor word of mouth at some destinations lead to a spillover effect, limiting medical tourism growth At times patients have faced difficulties in getting follow up treatment which is difficult to co-ordinate for some procedures at the home country. Limiting factors for outbound tourism from GCC Patients face difficulty in getting follow-up treatment in their home country after receiving medical treatment abroad Most medical tourism destinations are developing countries with limited legislation on malpractices in case of errors or complications Lack of transparency on costs, volumes and other information on clinical practitioners in some countries as well as cultural and language barriers. Germany, UK, US, India and Thailand are leading destinations for GCC medical tourists • Providers seeking and receiving accreditation from organizations such as JCI in order to alleviate concerns about quality of care. Hospitals are also getting accredited as certified medical tourism facilities from MTA and Temos. • Reputed medical institutions and providers collaborating with institutions abroad to create brand recognition for organizations and for the destination. • State health providers, ministries of health and big companies have recently launched plans that reimburse treatment costs in foreign locations, alleviating concerns about follow up care and coverage once back at home • Destinations like Thailand, US, India and Germany are providing concierge services and a cultural environment. • Destinations such as Turkey, Korea, Jordan & Malaysia are growing in popularity. …appears to be having an effect on patient sentiment Multiple surveys of patients’ experiences at facilities abroad suggest that most feel satisfied with the quality of care and would encourage friends and relatives to travel abroad for medical care Germany has an 87% satisfaction based on a recently concluded survey with 90% of patients who’ve sought treatment in Germany would recommend it to friends & family. Thank You [email protected]

© Copyright 2026 ExpyDoc