Advancing Life Cycle Economics in the Nordic Countries Kim Haugbølle, SBi –Danish Building Research Institute, Denmark (Email: [email protected]) Ernst Jan de Place Hansen, SBi –Danish Building Research Institute, Denmark (Email: [email protected]) Abstract Advancing construction and facilities management requires the ability to estimate and evaluate the economic consequences of decisions in a lifetime perspective. A survey of state-of-the-art on life cycle economics in the Nordic countries showed that, despite a number of similarities, no strong convergence of i.a. methodologies has occurred. Thus, a Nordic network of researchers, practitioners and authorities was established along with national networks. Within these networks, similarities and differences in approaches were explored. Three conclusions were reached. First, it was suggested that the configuration of the roles as client, owner and user is indicative of a client’s interest in life cycle economics. Second, a proposal for a common Nordic cost classification was put forward. Third, it was argued that there is a strong need to develop tools and methodologies to depict the cost/value ratio appropriately. Keywords: Clients, benchmarking, cost classification, value, life cycle cost 1. Introduction Facilities management is increasingly being recognised as an important strategy for improving building performance and optimising the economic return on investments. Although differences exist with respect to purpose, scope and priority, facilities management has now become a mature field with its own textbooks etc. [1]. An important element in facilities management is the ability to estimate and evaluate the economic consequences of decisions in a lifetime perspective. The potential for a significant reduction in facilities investment costs is demonstrated in e.g. post offices in Japan [2], and it is shown that life cycle operations, maintenance and recapitalisation costs over e.g. a 50-year life cycle represent the greater part of life cycle costs [3]. Nevertheless, the uptake of life cycle economics has been rather limited. The reluctant uptake has been explained by several factors. Among those are the fact that management focus is typically directed at the initial construction costs when making decisions about buildings [3], various types and quality of data [4], and a host of practical, behavioural and methodological difficulties [5]. 275 Recently, international convergence on methodology and cost classification has been sought by ISO (International Organisation for Standardisation). In relation to the ISO 15686 series on service life planning, Part 5 addresses whole life costing [6]. In parallel, convergence has also been sought on a Nordic level. Although the Nordic countries more or less share the same visions and methodologies regarding life cycle costing, different cost classifications and tools are in use [7]. Thus, the Norwegian government’s building and real estate agency Statsbygg together with the Danish Building Development Council, a Danish think tank, initiated a Nordic project in order to establish Nordic networks for knowledge exchange and to develop a common Nordic cost classification. The purpose of this paper is to report the findings of this project, which is further described in [8]. 2. Methodology The research methodology included data from three main sources: § A survey of state-of-the-art through visits and seminars in each of the Nordic countries during 1999-2001. § An extensive literature review based on searches in Nordic databases. § A dialogue approach based on six thematic Nordic workshops and a number of national network meetings during 2002-2004. 3. Typology of clients The client’s role is very important in relation to development, implementation and use of life cycle costing (LCC). Without an active and systematic demand for LCC from the client, the possibilities of LCC related considerations to make a break-through in the building sector are very limited. The client must possess a wide competence to handle planning, construction and operation of buildings. This puts focus on the client’s handling of the relations to all the stakeholders, i.e. the owner, the customers, the building sector and society (see Figure 1). The client’s handling of these four relationships requires different capabilities [9]: § Relation to the owner: The client must be able to estimate whether investments in a building project fulfil the estimates and demands for profitability and economic conditions that apply to the actual business ideas of the owner. The estimates will of course be different for e.g. social housing, governmental buildings or commercial facilities. § Relation to the customers: A prerequisite for the client’s work is knowledge regarding the wishes, needs and demands of the customer as well as the will and ability of the customer to pay. For both unknown and known customers, the client will be the one to crystallise and specify the requirements to the building. With unknown customers it 276 requires knowledge of the market, the supply situation and competition, the customers’ preferences etc. With known customers – e.g. inside own organisation – the ability to negotiate will often be needed to balance requirements versus costs and other consequences, etc. § Relation to society: The client must have knowledge of society’s requirements to both the building and to the client’s responsibility, as they are stipulated in laws, regulations, etc. The relation to society also includes handling public opinion, architecture and the environment in the broadest sense. § Relation to the building sector: The client’s purchase of services like design and construction from the building sector assumes an ability to formulate relevant requirements and to organise and manage the process including control and follow-up. The handling of the relations to the building sector put great demands on the legal competence as well as the client’s ability to handle risk. Owner Business idea Customer Users Society Client Laws Building sector Building process Figure 1: The relations of the client to the various stakeholders. Based on [9]. The Nordic project identified four trends that are changing the role of the client in the Nordic countries. Firstly, public clients increasingly have to operate on market conditions. Secondly, the ability of the client to handle demands and partners in the building sector that are often contradictory is becoming more critical in order to achieve better value. Thirdly, the corresponding national property indices based on the Investment Property Databank (IPD) have made it easier to compare the profitability of building investments. Fourthly, the behaviour of the users is increasingly being recognised as decisive for the operation of a facility. As stated by Bordass who discussed the costs and value of greener buildings and how they are perceived and assessed [10], a client’s adopting of life cycle costing or not in his practice will to a large extent depend on his incentives to pursue lifetime considerations. The incentives will in turn 277 be determined by how the role as client, owner and user is configured. Based on the Nordic project three different configurations were found to be possible: § Configuration 1 – client only: In this configuration, the client acts as a client only, and he does not occupy the role of neither owner nor user. Some clients may pursue lifetime considerations due to ethical concerns, but his economic incentive lies solely with fulfilling the task at hand –to deliver a building. Since the market pressure and the public regulation for lifetime considerations have notoriously been weak, he is rather unlikely to make lifetime considerations. Thus, this type of client was labelled the Hit-and-Run Client. § Configuration 2 – client-owner: In this configuration, the client will act as both a client and owner (or facility manager), but he will not be the end user of the facility. As Bejrum et al. [11] convincingly argued, the profitability of a facility lies in the right maintenance strategy. Thus, this type of client-owner could pursue lifetime considerations since he might have economic incentives to optimise the performance of the building in question. This type of client was labelled the Landlord Client. § Configuration 3 –client-owner-user: In this configuration, the client will act not only as a client, but also as both owner and user of the facility. This type of client would in principle have strong economic incentives to include lifetime considerations in his decisions, since he is building for his own use and has to pay all the costs. Therefore, he is likely to be interested in optimising the performance of the building in the long term. Thus, this type of client was labelled the Integrative Client. 4. Nordic cost classification For clients who wish to include lifetime considerations in their decision-making it is a prerequisite that costs are systematically and consistently collected, classified and validated. The Nordic countries have many years of experience in collecting various key performance indicators. However, classification of cost and the scope of each system have been different within each country. Thus, it was a major objective of the Nordic project to put forward a proposal for a common Nordic classification of costs. Obviously, the ongoing work on ISO 15686-5 [6] was closely followed. But ISO 15686-5 was discarded, because the terminology was perceived as inconsistent, the standard contained a mix of normative and informative elements, and the cost classification was too far away from practical experiences in the Nordic countries. Instead four other basic requirements were set up and pursued. First, a distinction must be made between (at least) three main groupings of costs associated with the acquisition of the building, the building related services, and the non-building related services (services related to the core business taking place in the building). Second, the three main groupings must be broken down into main services. To be able to maintain an overview, the number of main services should not exceed 10. Each of these main services could be broken down in more details if needed by the individual user, but it was 278 suggested that splitting into sub-categories should in principle follow the hierarchical structure shown below: § One-figure level indicates a main service e.g.: § Two-figure level indicates a specific service e.g.: 63. Waste handling § Three-figure level indicates an activity e.g.: 63.1 Internal transport 63.2 Compression § Four-figure level indicates a resource e.g.: 63.1.1 Equipment 63.1.2 Salary 6. CONSUMPTION Third, a cost classification should be based on existing systems and data e.g. the Norwegian standard NS 3454 [12], the classification used by Danish Facilities Management [13], and the Dutch standard NEN 2748 [14]. Fourth, experiences showed that the difference between ‘Operation’, ‘Maintenance’ and ‘Development’was not well understood in practice. Since the definitions of these services were critical with respect to negotiating maintenance budgets, to determine rent levels, tax regulations etc., special attention must be given to define these services. Table 1: Definitions of main services in the proposal for a common Nordic cost classification. No Main service Definition 1 CAPITAL All investments towards completion including decommissioning by the end of use of the facilities. 2 ADMINISTRATION Activities for administration, required payments and insurance costs. 3 OPERATION This account includes daily, weekly and monthly activities that are repetitive within a one-year period for building and technical installation systems that must satisfy given functional demands and requirements. 4 MAINTENANCE This account includes all activities and efforts put forward in a period of more than one year. For example, planned maintenance, replacement and emergency repairs, so that the building and technical systems satisfy the original level of quality and functional requirements. 5 DEVELOPMENT This account includes activities as a result of a change in the demand of core activities, the authorities, total refurbishment, or all activities to raise the construction standards in relation to the original level. 6 CONSUMPTION This account includes resources in terms of energy, water, and waste handling. 7 CLEANING All activities inside and outside needed to meet cleaning demands satisfactorily. 8 SERVICE All non-building related activities in support of the core activities. 279 The main services are defined in Table 1. ‘Capital’concerns all costs related to the acquisition of the building. ‘Service’concerns non-building related services. The remaining 6 main services are building-related services. In Appendix A, the classification of life cycle costs is described further on a two-figure level. Various activities are at present being undertaken in order to implement this cost classification. 5. Depicting the cost/value ratio The ability of the stakeholders to act in accordance with lifetime considerations depends among other things on whether useful methodologies and tools exist to depict the cost/value ratio. A number of different tools and methodologies from each of the Nordic countries and the experiences with their use in practice were scrutinised. In Figure 2 an overall typology of tools and methodologies are given. The list is not necessarily exhaustive. VALUE Investment Building process Operation and maintenance for MONEY Market analyses Cash flow analyses Value management Life cycle costing Customer satisfaction analyses Operation plan and budget Figure 2: Types of tools and methodologies. Two features were striking. First, the scope of most of the methodologies and tools focused on either value/quality or cost. Second, the application of most of the methodologies and tools focused on one overall phase in the building’s life cycle. Although some methodologies and tools could eventually overlap, the methodologies and tools would rather be complementary. Since the mutual integration of methodologies and tools was remarkably small, it would be difficult to assess whether the client got ”value for money”or not. Therefore, one of the great challenges in the future will be to develop tools and methodologies which can appropriately depict the cost/value ratio in order to guide more informed decisions. 6. Conclusions A Nordic project was carried out during the past three years in order to create a stronger convergence of life cycle economics in the Nordic countries. The purpose of the project was to establish networks for knowledge exchange and to develop a common Nordic approach to life cycle economics. Three conclusions were reached. 280 First, it is suggested that the configuration of the roles as client, owner and user is indicative for the interest of a client in life cycle economics. Three configurations were identified: 1. Client only – labelled the Hit-and-Run Client. 2. Client-owner – labelled the Landlord Client. 3. Clientowner-user –labelled the Integrative Client. Second, a proposal for a common Nordic cost classification was put forward. The proposal was based on, but extended, existing cost classifications and data. Costs were classified in 8 main groups of services: 1. Capital. 2. Administration. 3. Operation. 4. Maintenance. 5. Development. 6. Consumption. 7. Cleaning. 8. Service. Third, a number of tools and methodologies available to the construction and real estate cluster were scrutinised. The tools and methodologies were categorised according to their scope and application in the life cycle of the building. A striking feature was the relatively weak coupling of costs and value/quality. Thus, it is argued that there is a strong need to develop tools and methodologies that can depict the cost/value ratio more appropriately. Acknowledgements The authors would especially like to thank the co-editor of the final report [8] Svein Björberg (Multiconsult, Norway) and the co-authors Björn Marteinsson (Rabygg, Iceland), Christer Sjöström (KTH Gävle, Sweden), Sakari Pulakka (VTT, Finland), and Kirsten Lindberg and Stein Rognlien (Statsbygg, Norway). The authors also wish to thank Nordic Innovation Centre for financial support. References [1] Alexander, K. (1996). Facilities management – Theory and practice. London & New York: E & FN Spon. [2] Minami, K. (2004). Whole life appraisal of the repair and improvement work costs of Post Office buildings in Japan. Construction Management and Economics, 22, 311-318. [3] Selman, J. R. and Schneider, R. (2004). The impact of life-cycle cost management on portfolio strategies. Journal of Facilities Management, 3 (2), 173-183. [4] Kishk, M. (2004). Combining various facets of uncertainty in whole-life cost modelling. Construction Management and Economics, 22, 429-435. [5] Cole, R.J. and Sterner, E. (2000). Reconciling theory and practice of life-cycle costing. Building Research and Information, 28 (5/6), 368-375. [6] ISO (2002). ISO/DIS 1568-5 - Buildings and constructed assets - Service life planning Part 5: Whole life costing. Genève: International Organization for Standardisation. 281 [7] Haugbølle, K. (2003). Life cycle economics: State-of-the-art in the Nordic countries. In: ILCDES 2003: Integrated Lifetime Engineering of Buildings and Civil Infrastructures. Proceedings of the 2nd International Symposium, Kuopio, Finland, December 1-3, 2003. Helsinki: ILCDES 2003 Secretariat, 33-39. [8] Bjørberg, S. and Haugbølle, K., eds. (2005). LCC for byggverk. Nordisk hovedprosjekt – sluttrapport (LCC for Buildings and Constructions. Nordic main project - final report) (In Danish, Swedish and Norwegian with summary in English). Hørsholm: Danish Building Research Institute, (SBi 2005:01). [9] IVA (1997). Kompetensutveckling inom samhällsbyggnad. Byggherren i fokus (Development of competence in the building sector. The client in focus) (In Swedish). Stockholm: Royal Swedish Academy of Engineering Sciences (IVA). [10] Bordass, B. (2000). Cost and value: fact and fiction. Building Research and Information, 28 (5/6), 338-352. [11] Bejrum, H., Hanson, R. and Johnson, B. G. (1996). Det levande husets ekonomi. Livscykelekonomiska perspektiv på drift och förnyelse (The economy of the living house. The perspective of life cycle economics on operation and renewal of buildings) (In Swedish). Stockholm: SRB, Statens råd för byggnadsforskning. [12] NS 3454 (2000). Livscykluskostnader for byggverk – Prinsipper og struktur (Life cycle costs for buildings – principles and structure), Norwegian Standard, 2nd ed. Oslo: Norsk Standard. [13] Public website, http://www.dfm-key.dk [14] NEN 2748 (2001). Terms of facilities – Classification and definition. Dutch Standard. Delft: Nederlands Normalisatie-instituut. 282 Appendix A Classification of Life Cycle Costs 1 Capital Costs 11 Project costs This item includes all investments up to the finished construction. It can be subdivided into contractor costs (similar to enterprise costs), employee costs (fees, etc) and special costs (taxes, etc). It will be outlined that the contractor's costs can be divided into groups with the same rate of depreciation (see attachments). Land cost should be included. If this is a yearly fixed fee, it should be calculated to net present value. 19 Remaining costs Costs for elimination of construction at the end of its useful lifetime. This can also be the period of use. In some circumstances the remaining costs can be income. For example, the sale of the used construction materials for new projects or the whole building for new use. 2 Administration Costs 21 Taxes and fees 22 External fees 23 Administration and management 24 Insurance 29 Miscellaneous 3 Property tax and other required official fees (and independent expenditures) even if the structure is not in use. This item includes external assistance fees to the management, e.g. condition survey, legal assistance etc. Salary to administrative employees. It also includes rent of space for the use of management department, documentation of the construction inclusive the management of data based system for MOMD, the service desk, marketing, internal control, etc. This item includes fire and burglary. It also includes insurance for necessary building equipment to the management department. Casualty insurance and personal property of user is not included under this insurance. Example equipment for operation department. Operation Costs 31 Operation and Salary and all payments to employees (excluded are inspection executed by administration, see Account 2) including work clothing, materials own employees and equipment (includes car costs, trailers, etc), tools, etc. Work assignments worth mentioning: lubrication, adjustments and regulation of technical systems, fire protection, etc. including filters, bulbs, straps, etc. 283 32 Operation and This item includes all external agreements (service agreements) inspection executed by for operation and supervision of elevators, fire alarms, sprinkler external companies systems, ventilation systems, etc. 37 Outdoor operation and Salary and all payments to employees (excluded are inspection executed by administration, see account 2) including work clothing, materials own employees and equipment (includes car costs, trailers, etc), tools, etc. for snow removal, landscape services, operation of technical construction and systems, etc. (does not include parking buildings). 38 Outdoor operation and This item includes all outdoor works and agreements like snow inspection executed by removal, landscape services, operation of technical construction external companies and systems, etc. (does not include parking buildings). 39 Miscellaneous 4 Maintenance Costs 41 Periodical maintenance of exterior of the building 42 Periodical maintenance of internal of the building 43 Replacement of exterior This item includes work on the façade and roof that is necessary to prevent decay of normal wear and tear. 49 Outdoor Periodic maintenance and replacement of building components including technical systems i.e. fountains, asphalt, trees and bushes, fences and retaining walls. (Does not include parking buildings). This item includes work on the interior of the building to prevent decay with normal wear and tear, for example painting. This item includes work and efforts that are necessary in order to accomplish replacement of exterior building components (roofs and facades). Replacement is relevant when periodic maintenance no longer satisfy maintaining technical and functional demands (parts of the building that have shorter lifetime than the rest of the building). 44 Replacement of This item includes work and efforts that are necessary in order to interior accomplish replacement of the interior of the building. Replacement is relevant when periodic maintenance no longer satisfy maintaining technical and functional demands (parts of the building that have shorter lifetime than the rest of the building). 45 Emergency repair work This item includes work and efforts that are necessary to correct for exterior unforeseen situations. Includes emergency efforts to the façade and roof and aligning of damages. 46 Emergency interior This item includes work and efforts that are necessary to correct repair unforeseen situations. Includes emergency efforts to the interior and aligning of damages. 284 5 Developing Costs 51 Development and upgrading of exterior of the building This item includes costs for ongoing efforts caused by new demands from the authority or core business related. For example, new fire or environment regulations or core business related. Does not include total refurbishment*. 52 Development and This item includes costs for ongoing efforts caused by new upgrading of internal of demands from the authority or core business related. For the building example, new fire or environment regulations that gives retrospective force and thereby includes all buildings and simple rebuilding (moving doors, spatial walls, etc). Does not include total refurbishment*. 59 Development and upgrading outdoor This item includes costs as followed by demands from activity, the authority or in connection with total renovating that will elevate the quality. Does not include total refurbishment*. *: Total refurbishment (renovation) to accommodate new demands, new users, modernisation, etc. Is to be seen as new capital costs (a new project). 6 Consumption Costs 61 Energy 62 Water and Drainage 63 Waste Handling All costs related to energy supplies including oil, electricity and heating. All costs related to water consumption including intake water, waste water including cleaning This item includes all costs from internal transport, compression, source separation, collecting (hired container), transporting related to waste and taxes for landfill. 69 Miscellaneous 7 Cleaning Costs 71 Daily/Periodic 72 Main cleaning 73 Special cleaning 74 Window cleaning 75 Façade cleaning 79 Outdoor cleaning This item includes daily and weekly cleaning of all surfaces, including accessories and equipment. This item includes costs to periodic main cleaning, including accessories and equipment. This item includes, for example, floor waxing, etc. And includes accessories and equipment. Periodic interior and exterior window cleaning when this usually gets charged to the owner of the building or respective user. Costs for façade cleaning including all necessary help. Usually performed in connection with exterior window cleaning. This item includes cleaning of cultivated areas. Maintenance of green areas is not included. (See 3 Operation). 285 8 Service Costs 81 Security and safety Security outside the reception area during normal working hours. Boundary protection of the building includes operation of entry points, production of entry cards, etc. 82 Reception/switchboard Total salary costs include social benefits, uniform and service agreements. 83 Mail Total salary costs, postage, local transportation, operation and maintenance of the postal equipment. 84 IT service Total salary costs, operation and maintenance of all equipment. 85 Moving Total salary costs, transportation, extra maintenance and renovation. 86 Catering Total salary cost to in-house and/or contract personnel, operation of automated machines, products and articles of consumption of the kitchen and rent of space. 87 Accessories/copying Total salary costs, office and data accessories, internal and external copying, machines and equipment (rentals and service) papers, etc. 88 Administrative support Total salary costs for in-house or support personnel (doesn't include administrative personnel in main activities (core business)). 89 Furniture and Total salary costs, purchasing and depreciation of furniture and inventories inventory. Include rent of storage room. 286

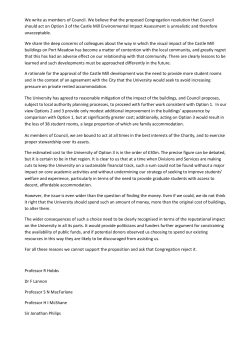

© Copyright 2026 ExpyDoc