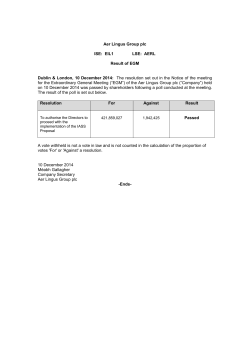

OEIC Investec UK Special Situations Fund An ideal fund to blend with the best in the industry? Citywire Scotland 2014 Why Investec UK Special Situations Fund? ● Strong historic risk-adjusted returns ● The Fund’s contrarian, value style blends well with funds of other investment styles ● Focused on identifying out of favour, cheap stocks with appropriate balance sheets ● Particularly strong historic performance in down markets ● Has typically bounced back quickly after underperformance ● Award winning and highly rated fund manager Page 2 | CONFIDENTIAL 18023 Investec UK Special Situations Fund A top long term performer 250% Investec UK Special Situations A Acc Net GBP 200% IMA UK All Companies FTSE All-Share TR 150% Percentage growth 211.2 100% 81.7 81.7 50% 0% -50% -100% Dec-99 Jun-01 Nov-02 Apr-04 Sep-05 Mar-07 Aug-08 Jan-10 Jul-11 Dec-12 May-14 Past performance figures are not audited and should not be taken as a guide to the future Source: Lipper, dates to 31 May 2014, NAV based, income reinvested (inclusive of management fees but excluding any initial charge) net of UK basic rate tax, in GBP. Fund ratings may be provided by independent rating agencies based on a range of investment criteria. For a full description of the ratings please see www.investecassetmanagement.com/ratings. Tenure since: 31 July 2002. Since launch: 10 October 1988 Page 3 | CONFIDENTIAL 18023 Period Sector ranking Quartile ranking 1 year 175/259 3 3 years 87/249 2 5 years 101/234 2 10 years 40/166 1 Tenure 28/144 1 Since Launch 9/44 1 Low correlation with other funds and high alpha over 10 years This chart illustrates the correlation of our outperformance against the FTSE All-Share Index with the outperformance of the average fund in the sector against the FTSE All-Share Index, compared with the alpha of the funds. 7.0 5.0 3.0 Investec UK Special Situations Alpha 1.0 -1.0 -3.0 -5.0 -7.0 -0.2 0.0 0.2 0.4 0.6 0.8 It indicates that the correlation of our outperformance is very low relative to most other high alpha funds (i.e. we outperform at different times to other high alpha funds) and that we are an ideal fund to blend with other funds to 1.0 create an optimal portfolio. Correlation Past performance should not be taken as a guide to the future, losses may be made. Data is not audited Lipper to 31 March 2014, annualised, NAV based, income reinvested (inclusive of management fees but excluding any initial charge) net of UK basic rate tax, in GBP. Correlation data are based on the relative returns of the funds in the IMA UK All Companies sector vs. the average fund against the FTSE All-Share over the ten year period to 31 March 2014. Chart axes converge on sector averages Performance refers to the A Acc share class Page 4 | CONFIDENTIAL 18023 A Fund that has protected clients’ wealth in falling markets 31.6 77.3 86.6 64.2 83.2 83.2 -45.4 -45.4 0 -5 -10 Percentage growth -15 -20 -25 -24.0 -30 -35 -40 -39.1 -45 -43.6 -46.4 -50 31-Dec-99 to 12-Mar-03 Investec UK Special Situations A GBP Acc Net 15-Jun-07 to 03-Mar-09 IMA UK All Companies FTSE All-Share TR Past performance should not be taken as a guide to the future, losses may be made. Data is not audited Source: Lipper to 25 June 2013, NAV based, income reinvested (inclusive of management fees but excluding any initial charge) net of UK basic rate tax, in GBP Page 5 | CONFIDENTIAL 18023 Performance necessary to return to break-even Why Investec UK Special Situations Fund? Alastair Mundy's UK Special Situations fund is one of the most effective ways to diversify your UK fund blend. This is as a result of its contrarian value bias which is relatively unique within the UK All Companies sector. Morningstar OBSR, April 2013 We believe the fund can fully complement a core investment in the UK and offer a good alternative to other styles in the UK All Companies sector. Rayner Spencer Mills, April 2013 Page 6 | CONFIDENTIAL 18023 Investec UK Special Situations Fund Current themes Will make it up as you go along central bank policy work? “As the Committee on this path [sic post 2009 policy], we were guided by some general principles and some insightful academic work but – with the important exception of the Japanese case – limited historical experience. As a result, central bankers in the United States, and those in other advanced economies facing similar problems, have been in the process of learning by doing.” Ben Bernanke, August 2012 Source: Federal Reserve website Page 8 | CONFIDENTIAL 18023 Debt remains a major problem It is still unclear how this corrects peacefully US Debt to GDP % 400 GSE Financial Corporate Household Public Debt remains very high 350 300 250 200 150 100 and government debt is now worryingly high 50 0 16 23 30 37 44 51 Source: Federal Reserve, Morgan Stanley Research, February 2014 Page 9 | CONFIDENTIAL 18023 58 65 72 79 86 93 00 07 14 How will governments meet their liabilities? Government liabilities to GDP % Why are investors so sanguine about government debt? Source: Société Générale Cross Asset Research, December 2013 Page 10 | CONFIDENTIAL 18023 US market as expensive on a forward P/E as its peak in 2007 Source: www.zerohedge.com, March 2014 Page 11 | CONFIDENTIAL 18023 The average stock is expensive Median ex-financial price to cash flow ratios in US and Europe Source: SG Cross Asset Research, June 2014 Page 12 | CONFIDENTIAL 18023 Far from perfect conditions for stock pickers Valuations across the US market have converged significantly Tight S&P 500 P/E dispersion relative to history Few opportunities for stock pickers Many opportunities for stock pickers Source: Goldman Sachs Global Investment Research , April 2014 Page 13 | CONFIDENTIAL 18023 Company profitability is high relative to history In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. Warren Buffett, 1999 Source: hussmanfunds.com, March 2014 Page 14 | CONFIDENTIAL 18023 US non-financial profit margins matching previous cyclical peaks Source: Credit Suisse, June 2013 Page 15 | CONFIDENTIAL 18023 Equity value is most apparent in large caps 4. Historical valuations by market cap 12 month forward P/E ratios 25x 20x 15x FTSE 100 10x FTSE 250 5x 0x Aug-98 Mar-00 Oct-01 Source: DataStream, as at 31 May 2014 Page 16 | CONFIDENTIAL 18023 May-03 Dec-04 Jul-06 Feb-08 Sep-09 Apr-11 Oct-12 May-14 QE and equities have been correlated…so far Source: Mauldin Economics, December 2013 Page 17 | CONFIDENTIAL 18023 But QE doesn’t mean equities must rise Commodities CRB index (rhscale) MSCI World Source: Société Générale Cross Asset Research, December 2013 Page 18 | CONFIDENTIAL 18023 Investec UK Special Situations Fund Current positioning Portfolio breakdown % weight No. of Stocks UK Equities 80.3 31 Internationally listed gold shares 0.5 5 Other internationally listed stocks * 8.0 7 Cash, Cash equivalents & Corporate Bonds 11.2 0 * The portfolio’s non-UK equity exposure is modified by short (i.e. seeking to benefit from a fall in value) futures positions held as follows: % weight Non-UK Equities (excl.gold shares) 8.0 Short S&P 500 futures -3.8 Net international equity exposure 4.3 Gross international equity exposure 11.8 ● Portfolio concentration: top 10 = 50.4%, top 20 = 72.1%, top 30 = 82.8% The portfolio may change significantly over a short period of time. This is not a buy or sell recommendation for any particular security Note: Excludes securities that individually account for less than 0.25% of the portfolio Source: Investec Asset Management, data as at 31 May 2014 Page 20 | CONFIDENTIAL 18023 Top ten holdings Security Royal Dutch Shell Plc Class B HSBC Holdings plc GlaxoSmithKline plc BP p.l.c. Unilever PLC Grafton Group Plc British American Tobacco p.l.c. Direct Line Insurance Group Plc Royal Bank of Scotland Group plc Tesco PLC The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular stock Source: Investec Asset Management, data as at 31 May 2014 Page 21 | CONFIDENTIAL 18023 Portfolio weighting (%) 8.6 8.4 7.4 5.6 4.3 3.6 3.5 3.2 3.0 2.9 Active positions Top 10 underweight positions Top 15 overweight positions Overwieght established 2004 Fund (%) 7.42 Index* (%) 3.71 Active (%) 3.71 Grafton Group 2008 3.61 0.06 Direct Line Insurance Group 2012 3.18 QinetiQ Group 2010 Unilever Security Vodafone Group Fund (%) 0.00 Index* (%) 2.65 Active (%) -2.65 3.56 AstraZeneca 0.00 2.55 -2.55 0.18 3.00 Diageo 0.00 2.30 -2.30 2.86 0.07 2.79 Lloyds Banking Group 0.00 2.01 -2.01 2003 4.29 1.54 2.75 Barclays 0.00 1.89 -1.89 Signet Jewelers Limited 2006 2.71 0.00 2.71 BHP Billiton 0.00 1.88 -1.88 HSBC Holdings 2009 8.36 5.72 2.64 Rio Tinto 0.00 1.82 -1.82 Royal Bank of Scotland Group 2012 2.97 0.35 2.62 Prudential 0.00 1.68 -1.68 SIG 2009 2.39 0.05 2.34 National Grid 0.00 1.58 -1.58 Carnival 2012 2.44 0.21 2.23 Reckitt Benckiser Group 0.00 1.57 -1.57 Tesco 2014 2.94 1.16 1.77 Chemring Group 2013 1.54 0.02 1.51 Kingspan Group 2009 1.47 0.00 1.47 CRH 2011 1.96 0.57 1.39 Go-Ahead Group 2009 1.41 0.04 1.36 Security GlaxoSmithKline The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular stock Data as at 31 May 2014. Source: Investec Asset Management * Index is FTSE All-Share Page 22 | CONFIDENTIAL 18023 Attractive 10 year risk vs. return 18 Annualised perf ormance % change 16 14 12 Investec UK Special Situations 10 8 6 4 2 0 10 12 14 16 18 20 22 24 Annualised standard deviation Past performance should not be taken as a guide to the future, losses may be made. Data is not audited Source: Lipper to 31 March 2014, annualised, NAV based, income reinvested (inclusive of management fees but excluding any initial charge) net of UK basic rate tax, in GBP. Chart axes converge on IMA UK All Companies sector averages Performance refers to the A Acc share class Page 23 | CONFIDENTIAL 18023 Shrinking to greatness ● Since the global financial crisis many companies have cut costs aggressively ● However, the very largest companies have been laggards here ● Large companies are now becoming more answerable to shareholders ● And more vulnerable to corporate activists and even bidders Page 24 | CONFIDENTIAL 18023 Investec UK Special Situations Fund Market-cap changes % of Equity Portfolio 90 FTSE 100 FTSE Mid 250 80 FTSE Small Cap/AIM/Fledgling 70 Intl Equities 60 50 40 30 20 10 Mar-07 Dec-07 Aug-08 May-09 Jan-10 The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular security Source: Investec Asset Management, data as at 31 May 2014 Page 25 | CONFIDENTIAL 18023 Oct-10 Jul-11 Mar-12 Dec-12 Aug-13 May-14 China remains the key source of industrial commodity demand Commodity consumption by country, % of global Source: Credit Suisse Equity Research, October 2013 Page 26 | CONFIDENTIAL 18023 The credit boom in China has been greater than most other credit booms Source: Credit Suisse Equity Research, October 2013 Page 27 | CONFIDENTIAL 18023 China's motorway density is greater than that of the US and the same on a per capita basis as the UK Source: Credit Suisse Equity Research, October 2013 Page 28 | CONFIDENTIAL 18023 Industry weightings Industrials Weighting Consumer Services Grafton Travis Perkins: Kingspan: Oil & Gas Health Care Technology Telecommunications Consumer Goods Financials HSBC and Royal Bank of Scotland held. No other bank holdings. Utilities 1.0% in gold miners Basic Materials -15.0 -10.0 The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular stock Source: Investec Asset Management, 31 May 2014 Page 29 | CONFIDENTIAL 18023 -5.0 5.0 10.0 15.0 3.6% 0.7% 1.5% Stock position changes 6 month period as at 31 May 2014 Tesco 2.94 BG Group 2.04 Royal Dutch Shell 1.36 Kingspan Group -1.36 Graf ton Group -1.65 BT Group -2.12 Signet Jewelers -2.15 Vodaf one Group -5.72 -7 -5 -3 -1 1 Change in position (%) Source: Investec Asset Management, FactSet, as at 31 May 2014 Page 30 | CONFIDENTIAL 18023 3 5 7 Sector position changes 6 month period as at 31 May 2014 Oil & Gas 5.15 Retail 1.63 Banks 1.36 Construction & Materials -1.29 Industrial Goods & Services -2.90 Telecommunications -8.40 -10 -8 -6 -4 -2 2 Change in position (%) Source: Investec Asset Management, FactSet, as at 31 May 2014 Page 31 | CONFIDENTIAL 18023 4 6 8 10 Why Investec UK Special Situations Fund? ● Strong historic risk-adjusted returns ● The Fund’s contrarian, value style blends well with funds of other investment styles ● Focused on identifying out of favour, cheap stocks with appropriate balance sheets ● Particularly strong historic performance in down markets ● Has typically bounced back quickly after underperformance ● Award winning and highly rated fund manager Page 32 | CONFIDENTIAL 18023 Investec OEIC UK Special Situations Fund Key facts Portfolio manager Domicile Fund structure Objective Performance comparison index Fund launch Fund size Share classes Ongoing charges Performance target* Alastair Mundy United Kingdom UK-based OEIC, Series i, UCITS compliant The Fund aims to provide a combination of income and long term capital growth, primarily through application of a contrarian approach to investment in UK equities and in derivatives the underlying assets of which are UK equities. FTSE All-Share 02 October 1978 £1,258.4 million (31 May 2014) A, S, I, B, J, R 0.84% (I-Share class) / 1.59% (A-Share class) 3% p.a. outperformance (gross) over rolling 3 years Source: Investec Asset Management, June 2014 * Performance target may not necessarily be achieved, losses may be made. Subject to change w ithout notification. Fund ratings may be provided by independent rating agencies based on a range of investment criteria. For a full description of the ratings please see w w w .investecassetmanagement.com/ratings. Align Page 33left | CONFIDENTIAL 18023 Thank you www.investecassetmanegement.com Appendix Investec UK Special Situations Fund Investment philosophy What is a special situation? We employ a disciplined investment process, making long-term investments in cheap, out-of-favour companies with appropriate balance sheets Out-of-favour Balance sheet/quality Page 37 | CONFIDENTIAL 18023 Cheap How do we identify contrarian stock opportunities? Company life cycles and share price cycles Earnings Growth Relative / Return on capital Tension zone In favour / expensive Overconfidence In trends Increased investment Fair value Cutting capacity Decline extrapolated indefinitely Company profitability Investor Behaviour Page 38 | CONFIDENTIAL 18023 Out-of-favour / cheap Tension zone Time Only significant long-term underperformers are highlighted by the screening process Stage 1 Stage 2 Stage 3 Stage 4 Share price relative to FTSE All-Share Index Relative price peak over last seven years excluding last two years 100 Must have fallen by at least 50% 50 -7 -6 -5 -4 -3 Time Page 39 | CONFIDENTIAL 18023 -2 -1 0 Investment process FTSE All-Share Index Mkt.Cap. > £200m Stage 1 Stage 2 Stage 3 Initial due diligence Valuation/Balance sheet/Structural risk Full analyst report Detailed company investigation Peer review Initial screen Post-screen analysis Fundamental research Stage 4 Analysis subjected to peer review Final due diligence Stage 5 Portfolio construction Buy & monitoring Page 40 | CONFIDENTIAL 18023 Stock universe Identifies out-of-favour stocks which have significantly underperformed over the long-term Investment team OEIC Cautious UK SS team – GBPteam – January (Linked2014 to Cautious Managed) Managed – GBP2014 – January ● Assembled from diverse backgrounds but united by contrarian ‘DNA’ Strategy Leader Alastair Mundy Investment Specialists Mark Wynne-Jones Celia Duncan Alessandro Dicorrado Peter Lowery David Lynch Steve Woolley Guillaume Redgwell Jessica Poon Portfolio analytics Jo Slater ● Team members are ‘out-offavour-company specialists’ employing cross-sector expertise – avoids biases and promotes fresh thinking ● Co-investment aligns individual and team interests with those of our clients ● £5.8 billion in assets under management* ● 16 years’ average industry experience, 8 years’ tenure * As at 31 March 2014 on a net sourced basis Page 41 | CONFIDENTIAL 18023 A Fund that has outperformed over bull markets 200 180 160 156.6 151.3 141.5 146.5 135.5 Percentage growth 140 124.8 120 100 80 60 40 20 0 12-Mar-03 to 15-Jun-07 Investec UK Special Situations A GBP Acc Net 03-Mar-09 to 22-May-13 IMA UK All Companies FTSE All-Share TR Past performance should not be taken as a guide to the future, losses may be made. Data is not audited Source: Lipper to 24 February 2014, NAV based, income reinvested (inclusive of management fees but excluding any initial charge) net of UK basic rate tax, in GBP The bull and bear markets are defined by the peaks and troughs in FTSE All-Share performance Page 42 | CONFIDENTIAL 18023 Attribution analysis 3 month top and bottom 10 attribution analysis to May 2014 Vodaf one Group PLC * Signet Jewelers Limited Unilever PLC Rio Tinto * Tesco PLC Lloyds Banking Group plc * Royal Bank of Scotland Group plc Johnston Press plc Helical Bar plc ARM Holdings plc * Avon Products, Inc. AstraZeneca PLC * CRH Plc GlaxoSmithKline plc SABMiller plc * SIG plc Kingspan Group Plc QinetiQ Group plc Chemring Group PLC Graf ton Group Plc 0.53 0.27 0.25 0.20 0.14 0.13 0.12 0.08 0.07 0.06 -0.10 -0.10 -0.12 -0.15 -0.16 -0.17 -0.18 -0.30 -0.34 -0.55 -0.8 -0.6 * Stocks indicated are not held on the fund The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular security Source: Investec Asset Management, 31 May 2014, vs. FTSE All-Share Page 43 | CONFIDENTIAL 18023 -0.4 -0.2 0.0 0.2 0.4 0.6 Attribution analysis 12 month top and bottom 10 attribution analysis to May 2014 Graf ton Group Plc Signet Jewelers Limited Kingspan Group Plc BT Group plc Barclays PLC * Direct Line Insurance Group Plc Tesco PLC Go-Ahead Group plc Helical Bar plc Vodaf one Group PLC Newmont Mining Corporation Associated British Foods plc * Lloyds Banking Group plc * Unilever PLC Prudential plc * Shire PLC * HSBC Holdings plc GlaxoSmithKline plc AstraZeneca PLC * Avon Products, Inc. 1.05 0.77 0.76 0.62 0.51 0.49 0.38 0.37 0.33 0.31 -0.16 -0.18 -0.21 -0.23 -0.26 -0.29 -0.42 -0.44 -0.45 -1.23 -1.5 -1.0 * Stocks indicated are not held on the fund The portfolio may change significantly over a short period of time This is not a buy or sell recommendation for any particular security Source: Investec Asset Management, 31 May 2014, vs. FTSE All-Share Page 44 | CONFIDENTIAL 18023 -0.5 0.0 0.5 1.0 1.5 Equity value is most apparent in large caps 1. UK Shiller P/E is in line with long-term average but skewed by the valuations of largest companies in the index? (Latest = 13.4x) Trailing Shiller Price to Earnings 35 30 25 20 15 Average 10 5 0 37 42 47 52 57 62 Source: Morgan Stanley Research Note: Shiller P/E defined as inflation adjusted price to 10Y average EPS Page 45 | CONFIDENTIAL 18023 67 72 77 82 87 92 97 02 07 12 Equity value is most apparent in large caps 2. FTSE 250 stocks are at the expensive end of their range FTSE 250 historical dividend yield 7 6 5 4 3 2 Source: Datastream, as at 31 May 2014 Page 46 | CONFIDENTIAL 18023 Dec-13 Dec-12 Dec-11 Dec-10 Dec-09 Dec-08 Dec-07 Dec-06 Dec-05 Dec-04 Dec-03 Dec-02 Dec-01 Dec-00 Dec-99 Dec-98 Dec-97 Dec-96 Dec-95 Dec-94 Dec-93 Dec-92 Dec-91 Dec-90 Dec-89 Dec-88 Dec-87 Dec-86 Dec-85 1 Equity value is most apparent in large caps 3. Valuations supportive of FTSE 100 relative to smaller companies Trailing price to dividends 60% 40% Premium/Discount 20% FTSE 100 vs. Small Caps 0% FTSE 100 vs. FTSE 250 -20% -40% -60% Dec-90 Aug-93 Source: DataStream, as at 31 May 2014 Page 47 | CONFIDENTIAL 18023 Mar-96 Oct-98 May-01 Jan-04 Aug-06 Mar-09 Oct-11 May-14 ‘Don’t fight the Fed’ – Why not? 2001-2002 market Source: www.hussmanfunds.com, 3 June 2013 Page 48 | CONFIDENTIAL 18023 2008-2009 market Private investor demand is high Annual net inflow to equity mutual funds and ETFs as % of the S&P 500 market cap Source: indecapital.com, November 2013 Page 49 | CONFIDENTIAL 18023 Contact details [] [] Tel: +44 (0) 20 7597 [ ] Email: [ ]@investecmail.com Investec Asset Management Woolgate Exchange 25 Basinghall Street London EC2V 5HA United Kingdom www.investecassetmanagement.com Telephone calls may be recorded for training and quality assurance purposes. Issued by Investec Asset Management, June 2014 Page 50 | CONFIDENTIAL 18023 [] Relationship Manager Tel: + 44 (0)20 7597 [ ] Email: [ ]@investecmail.com Important information Institutional Only This document is not for general public distribution. If you are a private investor and receive it as part of a general circu lation, please contact us at +44 (0)20 7597 1900. The information discusses general market activity or industry trends and should not be construed as investment advice. The economic and market forecasts presented herein reflect our judgment as at the date shown and are subject to change without notice. These forecasts will be affected by changes in interest rates, general market conditions and other political, social and economic developments. There can be no assurance that these forecasts will be achieved. Past performance should not be taken as a guide to the futur e, losses may be made. Data is not audited. Investors are not certain to make profits; losses may be made. The information contained in this document is believed to be reliable but may be inaccurate or incomplete. Any opinions stated are honestly held but are not guaranteed and should not be relied upon. This communication is provided for general information only and is not an invitation to make an investment nor does it constitute an offer for sale. This is not a recommendation to buy, sell or hold a particular security. The specific companies listed or discussed herein are included as representative transactions of the strategy. No representation is being made that any investment will or is likel y to achieve profits or losses similar to those achieved in the past, or that significant losses will be avoided. In the U.S., this communication should only be read by institutional investors, professional financial advisers and, at their exclusive discretion, their eligible clients, but must not be distributed to U.S. persons. In Australia, this document is provided for general information only to wholesale clients (as defined in the Corporations Act 2001). In Hong Kong, this document is intended solely for the use of the person to whom it has been delivered and is not to be reproduced or distributed to any other persons; this document shall be delivered to professional investors only. Investec Asset Management Hong Kong Limited is licensed by the Securities and Futures Commission in Hong Kong. Outside the U.S., telephone calls may be recorded for training and quality assurance purposes. Issued by Investec Asset Management, June 2014. Page 51 | CONFIDENTIAL 18023 Investec Asset Management Australia Hong Kong Taiwan Level 23, The Chifley Tower 2 Chifley Square Sydney, NSW 2000 Telephone: +61 2 9293 6257 Facsimile: +61 2 9293 2429 Suites 2602-06, Tower 2 The Gateway, Harbour City Tsim Sha Tsui, Kowloon, Hong Kong Telephone: +852 2861 6888 Facsimile: +852 2861 6861 Unit C, 49F, Taipei 101 Tower No.7, Section 5, Xin Yi Road Taipei 110, Taiwan Telephone: +886 (0)2 8101 0800 Facsimile: +886 (0)2 8101 0900 Botswana Namibia United Kingdom Plot 64511, Unit 5 Fairgrounds Gaborone Telephone: +267 318 0112 Facsimile: +267 318 0114 100 Robert Mugabe Avenue, Office 1 Ground Floor, Heritage Square Building Windhoek Telephone: +264 (61) 389 500 Facsimile: +264 (61) 249 689 Woolgate Exchange 25 Basinghall Street London, EC2V 5HA Telephone: +44 (0)20 7597 1900 Facsimile: +44 (0)20 7597 1919 Channel Islands South Africa United States PO Box 250, Glategny Court Glategny Esplanade, St. Peter Port Guernsey, GY1 3QH Telephone: +44 (0)1481 710 404 Facsimile: +44 (0)1481 712 065 Cape Town 36 Hans Strijdom Avenue, Foreshore Cape Town, 8001 Telephone: +27 (0)21 416 2000 Facsimile: +27 (0)21 416 2001 666 5th Avenue 37th Floor New York, NY 10103 US Toll Free: +1 800 434 5623 Telephone: +1 917 206 5179 Facsimile: +1 917 206 5155 Europe (ex UK) Johannesburg 100 Grayston Drive Sandown Sandton, 2196 Telephone: +27 (0)11 286 7000 Facsimile: +27 (0)11 286 7777 Woolgate Exchange 25 Basinghall Street London, EC2V 5HA Telephone: +44 (0)20 7597 1890 Facsimile: +44 (0)20 7597 1919 Please note that this communication is not necessarily approved for distribution in all of the above jurisdictions Page 52 | CONFIDENTIAL 18023 www.investecassetmanagement.com

© Copyright 2026 ExpyDoc