PCI REPORTER SUNDAY | 26 October 2014 LEAD SPONSOR PCI | OCTOBER 26-29 2014 | SCOTTSDALE, ARIZONA in association with PCI news and views are available LIVE and free from Apple Store and Google Play – search for Reactions PCI Reporter PCI with Reactions welcomes delegates to Scottsdale The leading luminaries of the US re/insurance industry were welcomed to Scottsdale this morning as delegates gathered for the Property Casualty Insurers Association of America’s (PCI) annual conference. More than 1,000 people are expected to attend this year’s conference, which brings together insurers, reinsurers and brokers, as well as service providers such as lawyers and claims companies, all of whom will be keen to listen to and discuss the most pressing issues facing the industry. TWO WORDS: PROFITABLE GROWTH PCI_Day1.indd 1 The theme of this year’s conference is “Leading in an Age of Disruptive Transformation”, and over the next few days the event’s agenda will give attendees plenty of opportunity to debate how the wider re/insurance industry will deal with the challenges it currently faces, as well as those looming on the horizon. “There are two things we hope to get out of the conference,” David Sampson, the president and chief executive of PCI, told Reactions. “We hope to facilitate contacts and transactions between our member companies – the primary insurers and then the brokers and reinsurers. That’s always a very important part of this annual event and we greatly value and appreciate all of the brokers and reinsurers who participate in it. We think it’s efficient and effective for our members first and foremost, but hopefully it’s good for the reinsurers and brokers as well.” The other element of the conference that Sampson believes is key relates to the education and information that PCI provides its members. The conference offers ➢ David Sampson Learn more at guycarp.com 25/10/2014 15:11 CONSIDERED DECISIONS? OR SPEED OF RESPONSE? WE’RE EXPERTS AT JUGGLING BOTH. We empower our underwriters to make decisions, without going round and round the circles of a hierarchy. We can do this because our underwriters are acknowledged experts in their spheres. Experts who can make decisions where – and more importantly when – they matter, based on a thorough understanding of your markets, their risks and your needs. Contact us at qatarreinsurance.com or better still meet us in person at one of the industry conferences. PCI_Day1.indd 2 25/10/2014 15:11 #PCIAM2014 Managing editor Peter Birks Tel: +44 (0)20 7779 8755 [email protected] Americas editor Christopher Munro Tel: +1 212 224 3473 [email protected] Senior reporter Victoria Beckett Tel: +44 (0)20 7779 8218 [email protected] Deputy editor Lauren Gow Tel: +44 (0)20 7779 8193 [email protected] Reporter Samuel Kerr Tel: +44 (0)20 7779 8719 [email protected] Contributing editor Garry Booth [email protected] Design & Production Nikki Easton Commercial director and publisher Gary Parker Tel: +44 (0)20 7779 8171 [email protected] Deputy publisher Goran Pandzic Tel: +1 212 224 3711 [email protected] Subscription sales executive Ben Bracken Tel: +44 (0)20 7779 8754 [email protected] Managing director Stewart Brown Tel: +44 (0)20 7779 8184 Email: [email protected] Divisional director Danny Williams Reactions, Nestor House, Playhouse Yard, London EC4V 5EX, UK www.reactionsnet.com Annual subscription rates Corporate multi-user rates are available. Please contact [email protected] Single user: £920 / €1,150 / US$1,475 Subscription hotline London: +44 (0)20 7779 8999 New York: +1 212 224 3570 Back issues Tel: +44 (0)20 7779 8999 Subscribers: £27.50; non-subscribers: £45.00 ISSN 0953-5640 Directors Richard Ensor (chairman), Sir Patrick Sergeant, The Viscount Rothermere, Christopher Fordham (managing director), Neil Osborn, Dan Cohen, John Botts, Colin Jones, Diane Alfano, Jane Wilkinson, Martin Morgan, David Pritchard, Bashar Al-Rehany, Andrew Ballingal, Tristan Hillgarth Customer services Tel: +44 (0)20 7779 8610 ©Euromoney Institutional Investor PLC London 2014 Although Euromoney Institutional Investor PLC has made every effort to ensure the accuracy of this publication, either it nor any contributor can accept any legal responsibility whatsoever for consequences that may arise from errors or omissions or any opinions or advice given. This publication is not a substitute for professional advice on a specific transaction. Reactions PCI Reporter | www.reactionsnet.com PCI_Day1.indd 3 Continued from page 1 ➢ attendees the chance to learn about the issues affecting the market, as well as a platform for discussion. “[At the meeting] we always try to help our members and CEOs look over the horizon and anticipate what’s next. What’s the world of risk transfer going to look like in the years ahead and what are the major factors that could impact that on a day in, day out basis? “These CEOs are very engaged in their companies and executing on their business plans, and we always try to make the conference an opportunity to step back from that micro look at running their companies and go up on the mountain top and survey everything that’s going on at a macro level to look at what’s coming at them.” As to what those challenges are, Sampson believes there are several issues at the top of the priority list for many of those in attendance. The future economic growth potential for the US and the wider global marketplace remains a concern, because, as Sampson explained, “that’s ultimately the driver of increased risk in the marketplace that needs to be transferred”. “Everyone is still very skeptical about the strength of the US economy, but also the slowdown globally that’s roiled the markets in the last couple of weeks,” he added. The turmoil currently affecting the Middle East is another issue for the re/ insurance industry to contend with, especially when considered in light of terrorism risk. This in particular links in to another concern for the US re/ insurance industry and the reauthorisation of the Terrorism Risk Insurance Act (Tria) which expires at the end of this year. “People are perplexed that something which has such broad bipartisan support in both houses of Congress is coming down to the wire in the lame duck session of Congress to be reauthorized,” said Sampson. “[That is creating] uncertainty in the marketplace at a time when there is clearly a resurgence of terrorism [and the] threat is as high as it’s been since September 11. Everyone is deeply concerned about that.” All these and more are sure to be on the agenda for those individuals at the PCI Conference in Scottsdale, and over the coming days Reactions is here to bring you the best insight and comment that emerges from the event. IN TODAY’S ISSUE 4 Berkshire Hathaway Specialty Insurance going global – Peter Eastwood 14 Soft market means greater volatility, Guy Carpenter finds 8 Emerging markets light the way 16 Munich Re holds firm, says Steven Levy 12 Innovate to succeed – Rod Fox 18 Time running out for Tria Sunday 26 October 2014 | 3 25/10/2014 15:11 @reactionsnet Berkshire Hathaway Specialty Insurance going global T he rapid growth enjoyed by Berkshire Hathaway Specialty Insurance (BHSI) since its launch is set to continue, with the company imminently moving into new lines of business and geographies. BHSI was officially launched on June 13 last year, but actually began life on April 29 2013, offering commercial property and casualty insurance cover to US-based clients. BHSI quickly increased its headcount from its initial team of four/five who moved from AIG (company president Peter Eastwood, and senior executives David Bresnahan, Sanjay Godhwani, and David Fields, with David Crowe joining BHSI soon after). Staff numbers are now at about 500, Eastwood told Reactions. Around 350 work within BHSI’s travel insurance business, a sector the company entered following the acquisition of Wisconsinheadquartered MyAssist and Insure America at the beginning of this year. The remaining 150 staff are engaged across BHSI’s seven other sectors: property, casualty, executive and professional lines, medical professional liability, surety, programme operation and homeowners. “Today, the majority of our business is in the commercial property and casualty space and I suspect it will be for the foreseeable future,” said Eastwood. “But we have a broad mandate and we can enter any part of the world and any product line we want as long as we feel we can generate an underwriting profit for Berkshire Hathaway. We have a significant amount of flexibility. Within the eight different product segments we’ve developed, we will be putting more product into the market and expanding our capabilities. That could be new products, entering new classes of business, or addressing the needs of a new customer segment.” While the US was the initial focus of Boston, Massachusetts-based BHSI, Eastwood said plans are in motion to open elsewhere. “Our business plan is to also build outside the US. We want to write indigenous business in the countries we enter – business which is profitable and where we can add value. We also want to satisfy the needs of multinational customers, whether they be US-based or a customer elsewhere in the world that has cross-border 4 | Sunday 26 October 2014 PCI_Day1.indd 4 exposures and an insurance need. We’ve spent a meaningful amount of time in 2014 taking the necessary steps to build the business in certain key geographies and working our way through the regulatory process to get the business registered and licensed from an insurance standpoint.” BHSI is now looking to enter into Hong Kong, Singapore, Australia, New Zealand and Canada. “In all of those locations we’ve begun to hire people and we are in varying stages of working through the regulatory process and being close to a position where we will write business,” said Eastwood. “Our objective is to build a long-term focused and diverse, both by geography and product line, principally commercial property and casualty insurance business. We’re now well underway to creating a global business.” As Eastwood explained, BHSI has done its best to offer as many products as it can in as short a time as possible. However, this has only been done when the company believes it can create an acceptable return for Berkshire Hathaway. “We’ve done our best to go wide as quickly as we can. We want to get a lot of product into the marketplace as quickly as we can with the belief that our distribution, our broker partners and the end customer want to build a strategic relationship with their insurance carrier. By going as wide as quickly as we can, we can satisfy as many of our customer’s needs as we possibly can. It’s a case of working across their business and not just on a specific lines, so we continue to build out more products underneath our eight broad product categories.” So far, the response to BHSI’s launch both from brokers and customers has been positive, Eastwood said. “I’m very satisfied with the progress we’ve made to date. We’ve been able to write a considerable amount of business in a fairly short period of time – we’ve now got approximately 2,000 customers. We’re looking to expand the relationships with each of the customers we currently have. As we acquire new customers, we want to sell them as much as we can.” Companies such as Swiss Re and Munich Re have said recently that they are looking to increase their participation in the specialty sector. Despite that, Eastwood believes there remain plenty of We have a broad mandate and we can enter any part of the world and any product line we want as long as we feel we can generate an underwriting profit for Berkshire Hathaway. Peter Eastwood, president, Berkshire Hathaway Specialty Insurance opportunities to write strong and profitable business over the long term. “Our business consists of a few principle assets: the balance sheet and the capital that it holds, the brand and the integrity it represents, and our people. Ultimately, brands are nothing more than a function of the actions of people over many years and we’ve got some demonstrated integrity within Berkshire Hathaway and within our team as well from past experiences at various companies.” “We can compete very effectively in the marketplace with the key assets that we have. Although I take nothing for granted, there’s still a tremendous amount of opportunity in the marketplace. We’re building a platform that, at its core, has simplicity over complexity. It’s about being a highly responsive organization and satisfying the needs of both the broker and the customer.” www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:11 #empoweredexpertise Something big... is happening in Insurance www.empoweredexpertise.com PCI_Day1.indd 5 25/10/2014 15:11 • SCOR SCOR sets sights on US reinsurance growth While some reinsurers are concerned at the possible opportunities for growth in the US, SCOR is confident its business plan will allow it to expand the amount of cover in writes in the region SCOR is broadening its horizons and targeting some of the largest insurers in the US as potential reinsurance partners following several years of expanding and diversifying its operations in the country. Recent years have seen SCOR grow its portfolio in the US by adding new clients to its original book of regional clients and by broadening the type and number of reinsurance protections it offers US insurers. “Building on its track record, SCOR has been carefully building its franchise in the US, expanding progressively its business appetite. We are now able to write significant shares of casualty, professional and large property accounts instead of just writing a small portion of these as we did before,” explained John Jenkins, SCOR USA’s treaty manager. “The fact that SCOR is one of the few Tier One global diversified reinsurers means we can work with clients across the board, from both a product standpoint and a geographical one. We can have a relationship with them across their business. It’s something we’ve been working on for the last couple of years and now we can supplement our traditional portfolio of regional and specialty companies.” The smaller and more specialist firms have been attractive to SCOR because they have a thorough understanding of their business. Indeed, as Jenkins explained, many outperform the wider market because they have such an in-depth knowledge of the market in which they operate. But SCOR is now also looking to provide reinsurance protection to some of the larger insurers within the US, Jenkins said. “A specialty operation that SCOR would have taken on seven or eight years ago would have been one that writes a single class of business. Now when we say specialty, we look at operations that specialise in large surplus and excess lines or have a large component of their business in that segment. “We think they’re great partner companies for us. We’ve looked through that entire segment of the marketplace and identified companies that do a really good job of working on the type of account they want to write, and on the underwriting and pricing that they do.” 6 | Sunday 26 October 2014 PCI_Day1.indd 6 This change in stance from SCOR comes at a time when the US reinsurance market is facing increased competition, with some companies looking to gain a foothold in the region for the first time while others are seeking to expand their existing presence. As such, there have been questions as to why SCOR would look to increase its commitment when pricing pressure is only expected to rise further in the short term. Jenkins observed many insurance companies are rethinking their attitudes towards how they buy reinsurance. With capital in plentiful supply, some insurers are increasing their retention and reducing the amount of risk transferred to the reinsurance industry. Other insurance companies, however, are changing the way they buy protection by cutting the number of companies within their reinsurance programmes. These insurers will have a programme made up of fewer, but stronger, reinsurers. Those firms looking to do this are those that SCOR is targeting in its bid to grow in the US. “For other reinsurers, this would be something that is seen as a threat as less reinsurance is being bought, but for SCOR it’s an opportunity to be on a programme that we haven’t been on before. Our decision to expand has been very well received by the market so far,” said Jenkins. One of the main reasons for this has been the recent trend of insurers looking to tier their potential reinsurance partners. Those at the top are the vast global multinational re/insurance companies while those further down the food chain will be companies restricted to particular geographies or product lines. “Our clients want to work with global reinsurers that can serve them across all of their product lines,” explained Jenkins. “Being one of the few reinsurers that is actually diversified around the world and in products, targeting the larger insurers has been a great initiative for SCOR because we’ve been able to expand the business we write for these companies. “SCOR has a good brand name and it’s well capitalised. We’ve also seen this trend with some of the larger insurers who are now purchasing John Jenkins, USA Treaty Manager, SCOR SCOR is one of the few Tier One global diversified reinsurers, which means we can work with clients across the board, from both a product standpoint and a geographical one these consolidated programmes as it simplifies the buying process for them. For us, not having been as big a player in this market, we view this new trend as an opportunity to get on programmes that we haven’t been on in the past.” This is all part of SCOR’s plan to grow its reinsurance business in the US. The Chicago office handles the bulk of the US treaty reinsurance business and is now home to around 70 staff, with more based in New York providing additional support and writing facultative covers. The US treaty business has almost tripled in the last seven years. “We feel we’ve brought together the teams in all the various disciplines and now we’re looking to grow that and build on it over time as we need to,” said Jenkins. “It’s a real growth opportunity for us.” www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:11 • Photo credit: Getty Images Over the past 50 years, s, the insurance and reinsurance industry has seen tremendous mendous changes. From products, services and distribution on networks to risk management, capital management andd regulation, nothing is how it used to be. Far from slowingg down, the pace of this change is accelerating. New technology nology is having a profound impact on the way in which wee assess, model, price and reserve risks. At SCOR, we have the andd expertise h experience i i to stay at the cutting edge of these developments. By sharing the art and science of risk with our clients, we can adapt to a changing risk universe together. scor.com PCI_Day1.indd 7 The Art & Science of Risk 25/10/2014 15:11 @reactionsnet Emerging markets light the way T he struggle for growth continues in the insurance markets of the world’s mature economies, six years on from the financial crisis. Meanwhile, across the southern hemisphere, from Latin America to South East Asia, continued strong economic activity in emerging countries keeps on fuelling the expansion of local insurance markets. Global non-life premium growth slowed to 2.3% in 2013, compared with 2.7% the year before, with total premiums at $2,033bn, according to a sigma study from Swiss Re. Not surprisingly, in view of economic conditions across North America and Europe, non-life premium growth was driven by the emerging markets. Non-life premium growth remained strong in 2013 in emerging markets at 8.3%, after 9.3% in 2012, and was solid across all regions with the exception of Central and Eastern Europe (CEE), the sigma report said. By comparison, non-life growth in advanced markets has been slow since the financial crisis in 2008. Premiums increased by an annual average of 0.7% between 2009 and 2013, compared with 1.9% in the period 2003-2007. Non-life premium growth in emerging Asian countries continued at 13% in 2013, on the back of sustained strong growth in China (+16%) that was based on rising motor sales and infrastructure investment. In Southeast Asia, Thailand premium revenues maintained momentum (+13%), despite lingering social unrest, while strong macro fundamentals underpinned insurance demand in Indonesia (+13%) and 8 | Sunday 26 October 2014 PCI_Day1.indd 8 the Philippines (+10%). In Vietnam, premiums were down 1.6% as the market recovered from the domestic financial turmoil of 2011–2012 related to corporate bankruptcy, when banks’ balance sheets deteriorated because of rising non-performing loans. In India, non-life premium growth slowed in 2012 to 4.1% from 8.9%, due to a weaker economy and poor business sentiment. But rising incomes and an expanding middle class will soon refuel demand for non-life insurance products in India, Swiss Re’s analysts believe. The non-life sector across the Middle East, Central Asia and Turkey has also developed well (4.7%), relative to its Western counterparts. Turkey, which produces over one quarter of the region’s premiums, grew by 13% mainly driven by a double-digit increase in motor liability business but engineering, property, credit & surety, workers comp and general liability premiums also expanded. In Latin America, despite a cooling economic environment, non-life insurance premiums ticked up by 7.2% in 2013 to $103bn, with Brazil, Mexico and Argentina leading the charge. Chile, Colombia and Venezuela all slowed as did Mexico, which is expected to keep trailing its peers. Rising tax rates and depressed consumer confidence in Mexico were behind sluggish growth in that market. Chile and Colombia also had weak growth in the motor and property lines, reflecting slowing economic growth and increasing competition. In Chile, harder rates after the 2010 earthquake attracted additional capacity into property insurance, which set the stage for the current soft market. In Peru and Colombia, resilient infrastructure investment should cushion the downside from softer private consumption, Swiss Re believes, while exposure to an accelerating US economy also bodes well for traderelated lines of business. Looking to the future, Shaun Crawford, Ernst & Young’s Global Insurance Leader, believes that the overall contribution of rapid-growth markets to insurance premium growth will continue to be very significant. “Some of the larger economies, such as Brazil, Russia, India and China, appear to have entered a period of slower growth but they continue to possess high, long-term potential. Crawford said in a report that new waves of market liberalisation and rapid consumer adoption of new technologies are opening additional markets such as Mexico and Thailand to non-domestic firms. “However, each market has its own distinct risk profile. Insurers will need to model the risks across all the geographies to clearly evaluate the drivers for growth and pick their targets carefully.” The E&Y report noted that many rapid growth economies have opened up their insurance markets over the years by privatising state-owned organisations, encouraging foreign investment and reducing tariffs and non-tariff barriers. It added that, while deregulation of the insurance sector has come relatively late in many emerging economies, reduced government intervention and the opening of domestic markets to global players created an array of attractive opportunities for the insurance industry. www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:11 #PCIAM2014 Insurers acquire a taste for MINTS “Insurers will need to model the risks across all the geographies to clearly evaluate the drivers for growth and pick their targets carefully” Shaun Crawford, Global Insurance Leader, Ernst & Young Reactions PCI Reporter | www.reactionsnet.com PCI_Day1.indd 9 Goldman Sachs Asset Management chairman Jim O’Neill was the first to coin the acronym BRICS to reference the fast growing economies of Brazil, Russia, India, China and South Africa. He has subsequently identified another set of countries with big potential: Mexico, Indonesia, Nigeria and Turkey – or the MINTs. But what makes the MINTs especially attractive to insurers? John Cusano, Accenture’s senior managing director of Global Insurance recently came up with the following suggestions. Mexico is close to the established markets of the US and the expanding markets in Latin America, and it’s growing well at 3.6%, without the drag of high population growth. Urbanization is expected to increase – a key indicator for insurance – while per-capita income is also expected to rise. Premiums are projected to grow by 13% thanks to economic performance. However, there are new capital requirements and tax law reform that could prompt industry consolidation. With GDP rising at 5.9% and low population growth of 1.4%, Indonesia is an attractive target for insurers. It’s already the world’s fourth most populous country, so low growth rates are good. Fairly low urbanization rates (53.7% projected for 2015) will increase to 72.1% in 2050, with a fast-growing middle class. Insurance penetration is low. Nigeria, one of Africa’s most populous countries, is urbanizing—and fast growing more wealthy. It has a substantial middle class and plenty of oil. Projected annual growth rates in non-life are 9.5% and 13.5% for life. Some big insurers are already purchasing existing Nigerian insurers as a way into this exciting market, Cusano said in his note. At 3.2%, Turkey’s growth is the least lively of the four, but its economic expansion continues apace driven by exports to the Middle East and a boost in investment spending. It’s already fairly well urbanized at 75.1%, a figure that is expected to rise to 87.3% in 2050. Another important indicator for insurance companies is the growth in wealth per capita from $7,274 in 2000 to $17,103 in 2013 (135.1%). Sunday 26 October 2014 | 9 25/10/2014 15:11 Following the arrival of its new management team in January 2013, Qatar Re, the global multi-line reinsurer headquartered in Qatar, has established a well-balanced and diversified portfolio that will provide the platform from which to pursue its goal of becoming a leading and globally recognised reinsurer. To this end, Qatar Re provides lead quotations and capacity across all international markets based on the in-depth technical and product expertise of its highly experienced underwriting teams. Its unique underwriting approach sees it measure the impact of each risk underwritten on the overall portfolio. This is coupled with a strong and growing capital base that is highly rated and offers instant diversification to reinsurance panels given its lack of correlation with traditional financial markets. Our underwriting team Qatar Re’s success is rooted in the quality and expertise of its team of highly experienced underwriting professionals who have an acknowledged track record in the industry. They provide a deep understanding of the markets in which they operate and an invaluable insight into the underlying trends based on many years of experience in the reinsurance sector. Qatar Re’s underwriters are empowered to make decisions enabling them to react quickly. The ability of clients and brokers to talk directly to the decisionmaker is an important cornerstone of Qatar Re’s business model and philosophy. Overview of the portfolio Over the past twenty months Qatar Re has built a global franchise, recruited a team of renowned underwriting specialists and established a global presence with its headquarters in Qatar, branch offices in Zurich and Bermuda and a representative office in London. Through a disciplined and selective approach to underwriting Qatar Re has grown its portfolio which continues to be well-balanced across its lines of business and territories. Qatar Re writes all major lines of property and casualty and specialty lines of business, including: Aviation & Space; Agriculture; Credit & Surety; Energy; Engineering; Liability; Marine; Motor; and Property. The focus on specialty lines is evident in its portfolio split. At present, Qatar Re’s largest specialty line of business is UK Motor (writing both proportional and nonproportional). Qatar Re’s success in this line has been aided by the company’s competitive advantage in the area of Periodical Payment Orders (PPOs) of which its Chief Actuary Mark Cockroft is an acknowledged expert. PCI_Day1.indd 10 25/10/2014 15:11 Agriculture is another line in which Qatar Re has established a strong presence, with this class business benefiting from strong worldwide growth and providing good diversification geographically (by region) and through uncorrelated sublines (e.g. multi-peril Crop, Hail, Blood and Livestock, Forestry, Aquaculture and Greenhouses). Qatar Re anticipates the average annual growth rate of the global agricultural insurance market to be in the range of 10 to 15% in the coming years, with increasing demand for both proportional and non-proportional reinsurance. An important addition to Qatar Re’s offering is Credit & Surety, with this line still enjoying reasonable growth. Qatar Re’s Credit & Surety underwriting team is in the process of rolling out its services to all key markets with the aim of developing a market leading portfolio written on a global basis. Thus far, the focus has been Gross written premiums Half Year 2014 by domicile of reinsured 3% on Continental Europe, complemented by business written in the Americas and Asia. Geographically, Qatar Re’s current portfolio has a strong bias towards Europe, followed by North America, the Middle East, Asia and Latin America. By mid-2014, and with a client base of more than 400 cedants, Qatar Re has achieved the critical mass and diversification required to build a capital-efficient global portfolio. For 2014, Qatar Re will meet the challenges of the current soft market cycle with a selective approach to underwriting and the drive to generate attractive risk-adjusted returns based on a holistic portfolio view. Despite the headwinds, Qatar Re is committed to its journey. Gross written premiums Half Year 2014 by lines of business Motor 3% 2% Property Agriculture 21% 17% Credit & Surety Europe 30% Americas 52% 25% Asia Africa Oceania PCI_Day1.indd 11 Energy 5% Marine & Aviation 6% 6% 17% 13% Engineering Others/Multi Lines 25/10/2014 15:11 @reactionsnet Innovate to succeed T igerRisk’s chief executive Rod Fox has seen a fair number of interesting times in the insurance and reinsurance industry, yet despite his long and distinguished career he finds the present an amazing time to be in the market. Highly competitive conditions, brought about by the entry of a variety of capital market players into the reinsurance industry, has meant that many reinsurers have been left searching for an advantage in order to differentiate themselves from other companies. This, Fox says, is creating a highly innovative atmosphere in the reinsurance marketplace. This new spirit of innovation is perhaps the most important theme in the market at the moment, changing an industry which can often be seen as too conservative. “I think it is a fascinating time for the business,” Fox told Reactions. “What we are seeing is a lot more innovation, and we are just scratching the surface on it. A little pet peeve of mine is that, in general, this can be a pretty staid and boring business. However, there is a lot of opportunity to innovate around the business. “I think we are now starting to see some of that, so that is interesting for me.” Fox says too much is made of the phrase “alternative capital” when reinsurers discuss the changing dynamics of the industry. He says that reinsurance is in its essence a business about providing capital and the fact that new capital is entering the business should not be seen as revolutionary or groundbreaking. This new influx of capital is driving the innovation that Fox now sees in the reinsurance industry, and he says that innovation is levelling the playing field between larger and smaller players, with ideas beginning to become more important than size. 12 | Sunday 26 October 2014 PCI_Day1.indd 12 “As more capital is coming in it is driving more innovation,” says Fox. “I think that is exciting and we are enjoying it and as a firm and we are thriving on it. “We are now close to seven years old, so it’s not like we are the new kid on the block, but we are finding that you don’t have to be huge to have great ideas. It’s a more level playing field now so it’s good.” Fox points out that the perceived threat posed to traditional reinsurers by the capital markets is not a new phenomenon. The capital markets have been involved in reinsurance investing for a number of years and will continue to be. However he says that perceptions may have changed about how committed new capital is to staying in the business long term. “It’s been around a long time,” Fox said talking about new capital. “My partner Jim Stanard brought alternative capital to Renaissance Re 10 to 15 years ago. It’s not a new phenomenon. “However, I think there is recognition that it is a part of the industry that is here to stay and I think also the recognition that there is dramatically more that can come in. “It is driving efficiency and people have to really figure out what their competitive advantage What we are seeing is a lot more innovation, and we are just scratching the surface on it. Rod Fox, chief executive, TigerRisk is as they go forward.” Additional capital in the market is something that worries a number of reinsurers. It scores highly on every survey about reinsurer concerns and is the talking point at almost all industry events. But Fox believes that the competition in the industry brought about by alternative capital, particularly in the catastrophe space, is forcing reinsurers into truly understanding their competitive advantage. This is healthy for the market and will allow for more innovation, forcing reinsurers to do better and more creative business, rather than focusing on just catastrophe lines where profits have been good. He says: “The other thing that I have talked about before is that everyone seems to focus on the catastrophe business, which is maybe only 10% of the global reinsurance market. But that’s the one that people talk about. “Reinsurers were generating outsized returns in the cat business and there is also a realisation that with all the additional capital those returns are getting more normalised.” Fox identifies specialty lines as an interesting play for the whole industry. He also notes that insurers now have to focus on writing better casualty business. “There are multiple levels of insurers going into specialty lines,” says Fox. “There are primary insurers delving into specialty lines and there are reinsurers paying more attention to specialty lines. There is a recognition that you can’t just make your living in the cat business. “I’ve also said for a couple of years that the industry has done a poor job selling casualty insurance. I don’t think the products have been particularly responsive and I don’t think we have spent enough time thinking through it. “I think there is more of that happening today on the casualty side of the business and I think we are just scratching the surface, so it’s exciting.” www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:12 Sirius Ad PCI_Day1.indd 13 25/10/2014 15:12 • @reactionsnet Soft market means greater volatility, Guy Carpenter finds M any underwriters may have reaped the rewards of a low level of natural catastrophe activity and modest loss development trends in 2013 by posting strong results, but a new report from Guy Carpenter and Oliver Wyman has found the insurance industry experiences a greater level of volatility in the midst of a soft market. The report, the fourth time the two Marsh & McLennan subsidiaries have jointly issued the Insurance Risk Benchmarks Research: Annual Statistical Review, shows that the relatively low level of natural catastrophe activity, impressive stock market returns, plus an increased level of benefits from deferred tax assets and changes to pension accounting all played a significant part in the strong financial results reported by property and casualty insurers at the end of 2013. Despite the ongoing concerns over the global economic situation and the soft market conditions that exist in many lines of business around the world, last year was a good one for many property and casualty insurers. Aside from the relative lack of natural disasters to hit the market and the insurance industry benefiting as a result, the report also found that the wider industry managed to continue its recent trend of reserve releases. Indeed, as the report shows, 2013 saw the property and casualty insurance industry record the largest release of the most recent accident year since 2007. At the same time, ultimate loss estimates were cut for each historical accident year since 2004. “Interestingly, the single-year reduction to estimated ultimate loss for the youngest accident year, 2012, was approximately 2% and represented the largest such decrease since 2007,” the report states. “The experience of the last three decades supports the view that the lines of business with highest concentration of bodily injury costs (general liability, products liability, and medical professional liability) present the largest uncertainty in initial reserve estimates. This highlights the need for reserve modules of economic capital models to consider the relationship between these liabilities and 14 | Sunday 26 October 2014 PCI_Day1.indd 14 Columbia University collaborated with Guy Carpenter and Oliver Wyman to produce the study macroeconomic drivers.” While many in the industry have been bemoaning the tough market conditions and how the influx of capital from a variety of sources across the sector has pushed down rates and pricing, the report, which the two Marsh & McLennan companies compiled in collaboration with Columbia University, shows insurers were able to secure rate and price rises in some select classes of business. “Companies have been successful at achieving rate increases and industry written premiums grew by 4.4%,” the report highlights. “Top gainers include workers’ compensation [up by 8.2% year on year], commercial auto liability [an increase of 7.7%], and products liability [which increased by 6.9%].” Rate increases in these lines of business have helped the industry maintain profits and revenues at a time when many other insurance classes are suffering from high levels of competition and increased capacity. But improvements in loss ratios have also played their part in ensuring insurers ended 2013 in a healthy state. Booked loss ratios for accident year 2013 are lower than the long term average for every line of business, the report explains. “In general, 2013 loss ratios compared favorably with those of recent years. Mild natural peril activity and modest trends in loss cost contributed to these results. Among the lines of business most favorably impacted were the two covering real property: homeowners and commercial multiple peril.” The tri-party report notes loss ratio volatility for the homeowners and commercial multiple peril segments “appears to be less than that for other lines of business”. However, as the report explains, that statement “should be interpreted with a grain of salt”. That is because the full range of potential natural peril losses is not extant in the loss history. Furthermore, because much of the volatility affecting these segments of the insurance industry stems from natural peril losses that are independent between years, the correlation with other lines of business is comparatively low. “These loss ratios exhibit strong dependence on regional market segment,” explains the report. “Companies in the Southeast/Gulf market segment have fared the worst. Northeast/Atlantic carriers seem to vary the most in terms of profitability and Midwest carriers are generally on the higher side.” It is the large, multi-regional companies that have the most success in the homeowners class of business, the report found. “Homeowner’s volatility is uncorrelated with other lines and driven by natural peril profile and geographic footprint,” the Guy Carpenter, Oliver Wyman and Columbia University study discovered. “The underwriting cycle is much less pronounced. Large, multi-regional companies have outperformed regional players and the key to stable profitability is regional diversification and risk management.” Looking at specific segments of the insurance industry, the report notes that private passenger auto loss ratios are the most stable in the industry. These do not appear to be materially better or worse in individual regions. At the same time though, this is a product that in recent years has become increasingly commoditized as competition has intensified. “The strongest loss ratio correlations have occurred between lines of business driven by trends in bodily injury costs, including general liability occurrence, products liability occurrence and medical professional liability occurrence,” the study found. “This suggests that risk models need to consider the common dependence of these claims on systemic drivers of loss cost.” www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:12 • GUY CARPENTER A.M. Best’s New Analytics Will Broaden and Improve P&C Industry Capital Modeling and Benchmarking of Tolerances A.M. Best’s rating analytics continue to evolve and the pace of change is accelerating as the industry embraces more analytical tools, emerging best practices, and peer benchmarking. The rating agency is placing greater emphasis on risk-based analytics in its ratings process and will increasingly focus on management’s ability to execute its business plans and reasonably deliver on its financial projections. The convergence of ORSA regulatory requirements and A.M. Best’s new emerging risk-based analytics has significant implications in 2015 and beyond. Large and small US P&C insurers will be expected to further develop their financial forecasting, capital modeling and risk tolerance metrics for both capital and earnings. Insurers will need to more tightly link their business plans, with both capital and earnings adequacy assessments from a risk-adjusted perspective, to maintain and enhance their Best’s Ratings while complying with new regulatory requirements. Insurers need to understand A.M. Best’s evolving criteria with respect to their company’s ratings and business plans, particularly in three areas: • Stochastic-Based BCAR (Best’s Capital Adequacy Ratio) • Earnings Adequacy & Variability • ERM Impact Analysis A Closer Look at Best’s New Analytics Stochastic-Based BCAR A.M. Best plans to refine its capital adequacy BCAR model and upgrade risk factors based on stochastic analysis. The change may negatively impact P&C insurers depending on their risk profile, rating levels, and capital position. A.M. Best is expected to publish a Draft Criteria Report early next year before implementing its Stochastic-based BCAR sometime in 2015. Implications of the new model include: • Stochastic-Based BCAR will incorporate a consistent TVaR risk metric and become A.M. Best’s risk-adjusted capitalization tool used in its ratings and capital evaluations Reactions PCI Reporter | www.reactionsnet.com PCI_Day1.indd 15 (l-r) Jack Snyder, Managing Director, Business Development and Head of the Rating Agency Practice, Strategic Advisory, Eric Simpson, Managing Director in the Rating Agency Practice and Mark Murray, Senior Vice President in the Rating Agency Practice, Guy Carpenter & Company, LLC going forward; Stochastic-Based BCAR will affect strategic risk-based decisions (including reinsurance) and accelerate industry trends of more companies developing their “own” internal financial/capital model, particularly among small to mid-sized insurers; • Certain insurers’ cost of capital will increase, especially for outlier companies that operate within industry lines exhibiting higher loss ratio/loss reserve volatility; exhibit aboveaverage company-specific loss ratio/loss reserve volatility; and have concentrated natural catastrophe exposures and asset risks. P&C insurers will need to understand these changes and how their risk profile and volatility impact their BCAR score and ratings. Negatively impacted companies will need to consider corrective underwriting actions and reinsurance solutions to address unfavorable BCAR scores and align their risk profile and risk tolerances to their desired rating levels. • Earnings Adequacy & Variability While “capital adequacy” remains important, a company’s ability to sustain acceptable operating performance is even more vital. The vast majority of P&C rating downgrades in recent decades for companies have been driven by “earnings adequacy” issues. Chronic under-performance erodes A.M. Best’s confidence in a company’s ability to execute its business plans and effectively compete. Insurers with sustained underperformance and greater earnings variability will be most at risk. Companies will need to think beyond “capital preservation” and develop “earnings adequacy” risk tolerance statements as well, given A.M. Best’s increased focus on a company’s earnings variability and financial forecasting. ERM Impact Analysis Analysts prepare ERM Impact scoring worksheets for Best’s Ratings Committee to gauge whether a company’s ERM capabilities support its risk profile and rating – and result in a ratings “lift” or “drag.” Companies will need to demonstrate that their ERM practice is linked to risk decisions, business plans, and financial forecasts. A.M. Best continues to view many insurers’ risk tolerance statements as needing further development and will be probing this topic more in rating meetings. Companies Will Need to Understand and Act Highly rated insurers will continue to develop their risk and capital management capabilities to gain a competitive advantage and improve their business performance. ORSA requirements and Stochasticbased BCAR are fast approaching. Together, they will accelerate companies’ need to better understand and “own” their risk profile and capital/ earnings risk tolerances. Guy Carpenter is fully prepared to assist our clients with these challenges. Sunday 26 October 2014 | 15 25/10/2014 15:12 @reactionsnet Munich Re staying disciplined in the face of competition C ompetition is the predominant issue affecting the US reinsurance market as alternative capital continues to take more business away from traditional reinsurers, says Steven Levy, the recently appointed president of Munich Re America’s reinsurance division. Steven Levy says the biggest issue facing reinsurers in the US is the current market competition that is driving reinsurance prices down. The segment that has seen most of this pressure continues to be property/catastrophe, traditionally one of the most profitable for reinsurers, says Levy. “This [competition] is driven by the ample capacity that is out there from both the traditional reinsurers and alternative capital. This comes along with the fact that many primary companies are also ceding fewer risks to reinsurers. “With respect to the alternative capital, it is mostly being channelled to non proportional catastrophe business, so that continues to be the segment that is experiencing the most pressure.” The squeeze on traditional property catastrophe business has caused a number of reinsurers to look at other lines of business, leading to fears in some quarters that the market will begin to lose its discipline as reinsurers scramble to look for new opportunities that provide more attractive pricing prospects. Levy says this will not be the case at Munich Re, which intends to maintain underwriting standards, despite the squeeze on prices. But this does not mean that the reinsurer will not look for other opportunities. “At Munich Re we continue to maintain our clear profit orientated underwriting policy despite pricing pressures, only accepting risk on a sound economic price and sound terms and conditions,” said Levy. “That being said, we are always on the lookout to offer innovative and tailored reinsurance solutions for our clients.” Casualty is an opportunity that continues to be trumpeted as a growth area for traditional reinsurers looking for more solid pricing opportunities. 16 | Sunday 26 October 2014 PCI_Day1.indd 16 Steven Levy While many other markets are starting to suffer similar pricing pressures from an influx of property catastrophe reinsurers entering new markets looking for better rates, Levy says casualty has remained relatively stable given the rate environment in the primary market which has in turn presented reinsurers with greater opportunities in the segment. “We are definitely seeing the reinsurers that were focused on the property cat space experiencing a lot of pressure because of alternative capital, given the focus of alternative capital on natural catastrophe excess of loss business. Those companies are diversifying into other lines, which is putting pressure on these other segments,” says Levy. “That being said, we are seeing greater stability in the casualty market. For example, pricing is still increasing in most primary segments for casualty, albeit in low single digits. And in casualty reinsurance, pricing still remains close to adequate. This is particularly notable compared to property segments, especially property cat excess of loss segment. “Many of our clients also continue to add casualty products to round out their product offerings, so we continue to see new opportunities for casualty, especially in the niche areas.” When analysing the benefits of traditional reinsurance over alternative capital solutions, reinsurers have been keen to emphasise that they offer far more than cheap capital. Traditional reinsurers insist that what they offer is a long-term partnership with cedents, and a guarantee to be there when they are needed in the wake of a disaster. This is the most frequent accusation levied at the alternative capital space, that when push comes to shove they are untested when it comes to paying out on claims and that in some cases there has been litigation when investors have been unwilling to part with their premium. “Clients frequently tell us that they really value the long-term relationships, they value dealing with parties who they are familiar with,” says Levy. “Clients know how we behave in stress scenarios whereas a lot of these things are unknown with alternative capital. “You have the whole experience with one cat bond sponsor and the litigation they experienced with their cat bond; compared with that we traditional reinsurers are in essence a known quantity.” “I think litigation is untested, there hasn’t been a significant event which has tested alternative capital’s willingness to pay claims or whether there will be issues in respect to that,” he continued. When looking at the market more broadly, Levy, like many in reinsurance, highlighted the global economy as one of the most important factors affecting the market, especially in the current low interest rate environment that continues to eat away at investment income. “Obviously the low interest rate environment is probably the most significant economic factor affecting the insurance and reinsurance industry,” Levy told Reactions. This is highlighted by the recent drop in interest rates and 10 year Treasury yields continuing to fall in October. “This obviously puts pressure on investment income and emphasises the need for underwriting profitability and discipline. “As a result sound technical underwriting remains key to maintaining stable profitability going forward. And that historically has been the focus of the Munich Re Group.” www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:12 PCI_Day1.indd 17 25/10/2014 15:12 @reactionsnet Time running out for Tria T he Tria programme expires at the end of December, and if it is not renewed imminently, many industry experts are speculating that it will severely affect the terrorism insurance market in the US. Even by Washington standards, the renewal process this time around has been arduous. Despite a deal looking close after the Senate passed an extension in July, differences of opinion in the House led to a halt in negotiations in the lower chamber. The insurance industry had been hoping for a relatively straightforward extension of the programme for a number of years, but recent murmurings in the House have suggested that this may not end up being the case. “It’s going to get extended. The question is, do you do reforms now and negotiate, or do you just do a short-term extension into next year and then negotiate reforms?” said Rep. Paul Ryan (R-Wis.) on September 18. “You will not see just a straight current law extension.” There remains a possibility that, if the Republicans win the Senate in November’s midterms, then some members of the House might wish to revisit the issue again when both Houses in Congress are controlled by their party next year. “There is an uncertainty over whether the US Senate will go Republican after the election which could change the dynamics. If the House is looking at a Republican Senate next year it may feel that it would prefer to take up the issue in 2015 when both Houses are of the same political persuasion,” Bob Hartwig president of the Insurance Information Institute (III) told Reactions. This may be the view of some Republicans in the House and it certainly would make a short-term extension of the kind that Ryan has suggested more likely. 18 | Sunday 26 October 2014 PCI_Day1.indd 18 There is an uncertainty over whether the US Senate will go Republican after the election which could change the dynamics. Bob Hartwig, president of the Insurance Information Institute However, a Republican senate would not necessarily be in favour of the kind of extension that failed in the House in July. As has been a welldocumented scenario, the GOP is entwined in an ideological battle between the mainstream and the more conservative wing of its party. In the House, the main force behind modifying Tria has been Jeb Hensarling (R-TX) Chairman of the House Financial Services Committee. Hensarling sits on the ideological right of the GOP, and has in the past expressed relative disdain for Federal government involvement in private industry, including insurance. This has led the committee to propose a rise in the programme’s loss trigger, shifting more responsibility to the private market. On the other side of the GOP are more pro-Tria Republicans vocally represented by Rep. Peter King (R-NY), who has publicly dismissed any attempt made by Hensarling’s committee to modify Tria or raise the programme’s loss trigger. This would likely diminish industry capacity for terrorism insurance as a raised loss trigger could force smaller insurers out of the market. The majority of the House of Representatives is thought to favour the bill being proposed by the Senate, but it is Hensarling’s House Financial Services Committee that is responsible for bringing a bill to the floor of the House. The fact that the House failed to pass the House Financial Services Committee bill would suggest that there is not widespread support for a heavily-modified version of the programme among Republicans. This is also backed up by the overwhelming support for the bill in the Senate, 94-3 in favour of a straight extension. A Republican majority in the Senate doesn’t change the fact that most Republicans in Congress like the programme as it is. However, the key to a quick success here will be working with Hensarling, who has been accused of stubbornness in the past, on a compromise rather than fighting him. Those closest to the negotiations are still optimistic of a deal being struck during a Lame Duck session and there is significant momentum in both parties to get this done. “I know that the leadership on both sides of the aisle are prepared to have this be an item in a Lame Duck session and I think the challenge now is to keep the pressure on so that a deal is ready to be made,” said Leigh Anne Pusey president and chief executive (CEO) of the American Insurance Association (AIA) told Reactions on the last day the House was in session. “I was with Chairman Neugebauer [chairman of the Insurance subcommittee on the House Financial Services Committee and a close ally of Hensarling] this morning and nobody wants to get this deal done more than he does and he has spent a lot of time getting this bill in better shape than I think a lot of us expected that we would get out of the House.” The only thing likely to hinder Tria would be a return to some of the intransigence that has been associated with Washington over the past couple of years. www.reactionsnet.com | Reactions PCI Reporter 25/10/2014 15:12 DON’T IMPLEMENT YOUR ENTERPRISE RISK MANAGEMENT PRACTICES IN THE DARK. At Standard & Poor’s Ratings Services, our experience in the Insurance sector has led to the launch of our Enterprise Risk Management (ERM) Benchmark Review, a new stand-alone product providing insurance companies with a comparison of their ERM practices against their peers and our criteria. Our ERM Benchmark Review also helps insurers keep up with emerging risks and trends, such as the 2015 ORSA reporting requirements mandated by the NAIC, climate change and cyber risk. To learn more, contact Steven Cooke, Senior Director, Client Business Management at 212-438-7240 or [email protected] The analyses, including ratings, of Standard & Poor’s and its affiliates are opinions and not statements of fact or recommendations to purchase, hold, or sellsecurities. They do not address the suitability of any security, and should not be relied on in making any investment decision. Standard & Poor’s does not act as a fiduciary or an investment advisor except where registered as such. Copyright © 2014 by Standard & Poor’s Financial Services LLC. All rights reserved. www.SPRatings.com/ERM STANDARD & POOR’S and S&P are registered trademarks of Standard & Poor’s Financial Services LLC. PCI_Day1.indd 19 25/10/2014 15:12 TWO WORDS: PROFITABLE GROWTH Guy Carpenter Strategic Advisory uses our insights to integrate your capital and risk objectives into an equation for profitable growth. Our global team of over 150 leading experts in the areas of business expansion, capital advice and structuring, advanced analytics and industry and market intelligence work together seamlessly to customize integrated advisory and implementation solutions for our clients. GUY CARPENTER Learn more at guycarp.com STRATEGIC ADVISORYSM GROWTH | CAPITAL | RISK | INSIGHT PCI_Day1.indd 20 25/10/2014 15:12

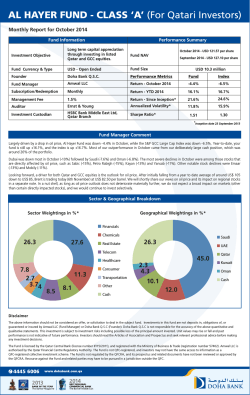

© Copyright 2026 ExpyDoc