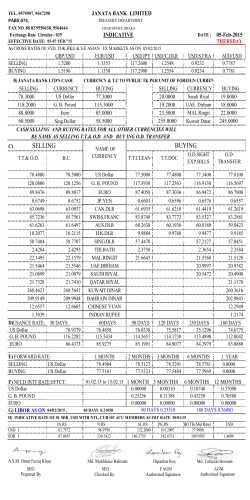

NOVEMBER 2014 NAV $103.16 (I) Share Class INVESTMENT OBJECTIVE The Fund aims to achieve steady income and capital growth by investing in local and hard currency bonds of African sovereign and corporate issuers. The Fund is benchmarked at rolling 1 month $ Libor +5.00% per annum, and aims to generate positive risk-adjusted returns for investors in all market environments. INVESTMENT STRATEGY The Fund invests predominantly in African hard and local currency sovereign bonds, as well as bonds from Supranational issuers in local African currencies. Corporate bonds will be added to the portfolio opportunistically, and as corporate bond markets evolve over time across Africa. The Fund is an actively managed long-only strategy which cannot avail of leverage. Hedging of currency, interest rate and credit risk is allowed and will be employed if and when deemed feasible. Capital preservation is a cornerstone of the Fund strategy. While a diversified portfolio across countries and currencies and the availability of hedging instruments in core markets should help to limit downside risk, the Fund Manager reserves the right to allocate a substantial part or all of the portfolio to conservative instruments such as U.S. Treasuries in times of stress. RISK CONSTRAINTS The Fund’s risk constraints are designed to limit concentration risk for the country and currency allocation, while providing flexibility to the Fund Manager when rotating between different markets and instruments. The Fund currently cannot invest more than 35% in any country (exclusive United States) and not more than 30% in any single currency (exclusive U.S. Dollar). If investing in Corporate Bonds, a maximum of 30% can be allocated to Corporate or Financial issuers as a group, while individual Corporate or Financial issuer exposure is capped at 5%. All requirements are inclusive of cash. FUND MANAGER’S REPORT As at 28th of November 2014, the NAV of the (I) share class stood at $103.16, representing a gain of 0.08% for the month. Standard Bank Africa Sovereign Bond Total Return Index gained 0.43%, mainly driven by a continuing rally of the long end of the U.S. Treasury yield curve. Yields on 10 year U.S. Treasuries declined by 0.17% during the month. Spreads were volatile but had an overall neutral performance . An inaugural Eurobond issue of Ethiopia was rumored to come to the market in the beginning of December 2014. Kenya tapped its outstanding 5 year and 10 year Eurobond issues by $250 Mio and $500 Mio, respectively, putting some pressure on secondary market prices towards the end of the month. That said, a bid/cover of 4x suggests continued confidence by international investors for the credit. In the local currency debt space, currency losses were eating into carry across the board. Despite regular interventions by the central bank, the Shilling depreciated further by almost 1% during the month, while the Ugandan Shilling lost 2.5%. Yields in Kenya remained stable, but in Uganda 1 year T-bill yields approached 14% in primary markets, and should be expected to rise further if the local unit remains under pressure. As inflation remains firmly under control, real yields on local currency debt in Uganda become even more attractive, but as long as currency markets do not stabilize it is hard to expect yields to edge lower. No direct intervention in currency markets by the central bank has been witnessed in Uganda so far. USD/RWF remained overall stable, despite the ambiguity on an eventual 3rd term of Paul Kagame, which is considered to be an anti-constitutional move. New 7 year local currency debt of Rwanda could be placed at 12.50% during the month. USD/ZAR rose by 0.21% in a roller-coaster ride during the month, with fears of a credit rating downgrade still lingering. The pair is not far away from its all-time highs. Interestingly, the long end of the SA government bond curve decoupled somewhat from movements in the currency. USD/ZMW remained overall capped at 6.40, which is quite remarkable given the dispute in the ranks of the Patriotic Front between Acting President Scott and Justice Minister Lungu, who was elected as new leader of the party following the death of late President Sata. Pressure on the Kwacha is rising though as markets remain quite illiquid. In West Africa, USD/GHS fell by 0.75%, despite expectations that the IMF balance of payment support scheduled for January 2015 will be delayed due to on-going negotiations. The West African Franc followed broadly the movement of EUR/USD, its peg, depreciating slightly in November. The new 7 year sinkable government bond issue of Senegal was successfully placed at a yield of 6.50% by the lead managers. Nigeria was the focus in our universe in November, as the Naira shed 8% and local equities were hammered as well. To accompany repeated FX market interventions that failed to stem the slide in the currency, the central bank increased the monetary policy rate by 1.00% to 13.00%, moved the naira’s official peg to NGN168/US$ and tightened liquidity in the interbank market. Yields across the curve rose consequently. At the end of November, 1 year non-deliverable forwards (NDFs) on USD/NGN traded around 200.00, with implied yields around 20% indicating further depreciation risks. While some market participants start to lock in those levels, sometimes as a switch against existing bill and bond positions, an official devaluation of the Naira even before the elections in February 2015 cannot be ruled out now. Only a relief rally in crude oil driven by elevated short covering could temporarily improve the sentiment for Nigeria. Apart from the new Ethiopia Eurobond issue, the month of December should mainly see rebalancing operations on the back of new inflows into the fund. The rumored Eurobond issues for Uganda and Tanzania will most probably not materialize in 2014. The local currency space remains difficult given the overall USD strength and negative performance of Emerging Market currencies across the globe. New positions should only be expected on exceptional opportunities until the end of the year. An engagement in the battered Nigerian bond market is not planned for the time being. MONTHLY PERFORMANCE SINCE INCEPTION 2014 JAN - FEB - MAR - APR - MAY JUN JUL AUG SEP OCT NOV 0.09% 0.44% 0.40% 0.81% 0.77% 0.54% 0.08% DEC YTD 3.16% TOP FIVE HOLDINGS NOVEMBER 2014 Instrument Country Rating Weight SENEGL 6.50% 11/2021 Senegal B+/B1/- 11.1% IFC 12.25% 05/2019 Supranational AAA/Aaa/AAA 8.5% SENEGL 6.25% 07/2024 Senegal B+/B1/- 5.2% IVYCST 5.375% 07/2024 KENINT 6.875% 06/2024 Ivory Coast -/B1/B 5.0% Kenya B+/-/B+ 4.7% FUND MANAGER PORTFOLIO STATISTICS IPRO Fund Management Ltd 28 November 2014 Modified Duration Yield to Maturity 31 October 2014 2.31 7.08% 2.78 7.49% INVESTMENT ADVISOR IPRO Botswana (Pty) Ltd FUND PARTICULARS COUNTRY ALLOCATION 16% Senegal Kenya Ghana Supranational Zambia Uganda Ivory Coast Rwanda Liquidity 32% 12% 2% 5% 11% 7% 7% 8% FEES & ADDITIONAL INFORMATION CURRENCY ALLOCATION 6% USD XOF RWF GHS UGX ZAR ZMW KES Open ended fund, domiciled in Mauritius, under IPRO Funds Ltd Fund Size: $5.9 million (28 November 2014) Inception date: 13 May 2014 Base Currency: USD Minimum Investment: $1,000,000 Increments: $100,000 Dealing Frequency: Weekly (the first Business day following Valuation day) Share Class Code: AAR-I-USD Information Memorandum: November 2008 Distribution Policy: Interest payments reinvested Investment Manager: IPRO Fund Management Ltd Domicile: Republic of Mauritius Custodian: Standard Chartered Bank (Mauritius) Ltd. Administrator: Galileo Portfolio Services Ltd. Auditors: BDO & Co. Valuation Day: Weekly Registered for sale: Mauritius Initial Entry Fee: up to 2% Annual Management Fee: 1.25% T.E.R.: 1.95% (indicative) Annual Performance Fee: 10% of outperformance against rolling 1 month $ Libor + 5.00% (waived for first 12 months after Inception Date of the Fund) Exit Fee: up to 5% for redemptions within 12 months of subscription (payable to the Fund) 3% 3% 7% 7% 52% IPRO MAURITIUS 10% Investment Professionals Ltd, 3rd Floor Ebène Skies, Ebène, Mauritius Tel : (230) 403 67 00 Email: [email protected] (Stéphane Henry, CEO) Web: www.ipro.mu 12% FUND PERFORMANCE IPRO BOTSWANA MTD YTD ISIN AAR (I) 0.08% 3.16% MU0344S00020 Bloomberg n/a Lipper Morningstar 65145411 n/a IPRO (Botswana) Pty Ltd, Unit 3, Plot 115, Kgale Mews, Gaborone International Finance Park, P/Bag 351, Suite 472, Kgale View Postnet Gaborone, Botswana Tel: (267) 316 5472/3 Email:[email protected] DISCLAIMER AND IMPORTANT INFORMATION Risk factors you should consider bef ore investing: •The value of shares and the income from them can go down as well as up and you may get back less than the amount invested. • Past performance is not a guide to the future performance of the fund. • Movements in exchange rates can impact on both the level of income received and the capital value of your investment. If the currency of your country of residence strengthens against the currency in which the underlying investments of the Fund are made, the value of your investment will reduce and vice versa. • The Fund invests in emerging/frontier markets which tend to be more volatile than mature markets and the value of your investment could move sharply up or down. In some circumstances, the underlying investments may become illiquid which may constrain the Investment Manager’s ability to realise some or all of the portfolio. The registration and settlement arrangements in emerging/frontier markets may be less developed than in more mature markets so the operational risks of investing are higher. Political risks and adverse economic circumstances are a reality, putting the value of your investment at risk. Asset allocations are subject to change and yields may fluctuate. This document is not an invitation to subcribe to the fund, and should be used f or inf ormational purposes only.

© Copyright 2026 ExpyDoc