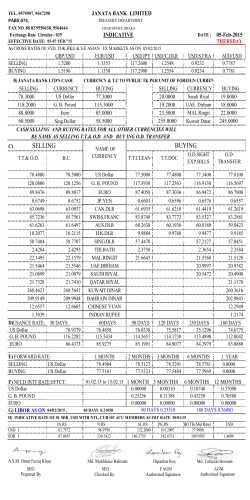

GLOBAL FX STRATEGY DAILY FX UPDATE Camilla Sutton, CFA, CMT Chief Currency Strategist (416) 866-5470 Eric Theoret, CFA, CMT Currency Strategist (416) 863-7030 Friday, February 6, 2015 [email protected] [email protected] FX QUIET, WAITING FOR PAYROLLS USD—flat vs all but EUR & AUD; consensus expecting 230K for NFP. CAD is unchanged ahead of dual jobs release; 5K gain expected. EUR weakens in response to industrial data from Spain & Germany. GBP flat, showing greatest weekly gain since February 2014. CHF consolidates; SNB reserves at 498bn as of January. USDJPY quiet, constrained by fundamentals & broader tone. AUD rallies in response to RBA quarterly Statement report, despite modest delay to anticipated recovery & growth drivers’ transition. CNY strengthens as PBOC fix rises most since November. FX Market Update - Markets are quiet ahead of payrolls, with most of the G10 currencies consolidating vs the USD, with the exception of fundamentally-driven weakness in EUR and outperformance in AUD following the release of the RBA’s quarterly Statement on Monetary Policy. The broader market tone is mixed, with equity futures hinting to modest gains as gold softens while the U.S. 10Y yield consolidates just above 1.80%. Commodities are divergent, with gains in oil prices offset by an accelerating decline in copper. Focus through the NA session will center on the U.S. employment release (discussed below), with voting Fed dove Lockhart scheduled to speak at 12:45pm EST. E.T. Nonfarm payrolls and the USD—consensus is calling for job gains of 230k, just below the six month moving average of 264k, with estimates ranging from 180k to 286k. Recent U.S. economic data has been uneven, helping to push expectations for the first Fed interest rate increase out to the October 28th meeting. The USD and interest rate expectations are always sensitive to the nonfarm payrolls print, which will hold again today, particularly because of recent market volatility combined with building anxiety over the strength of the U.S. recovery. Our summary of the USD reaction is below: An above expected print (+250k): is likely to see the USD rally between 50 and 100 points against most currencies; A slight miss (210 to 230k): is likely to drive a slight USD drop—30 points; A significant miss (below 200k): could see further USD long covering and drive a more material downside drop. Developments on the wage front will also prove important, with a increase in wages supporting the current Fed stance. C.S. USDCAD (1.2444) • CAD is unchanged ahead of the employment release (discussed below), consolidating vs the USD at the upper end of its one week range. CAD remains highly sensitive to movement in oil prices (see top chart), with the latter now directly influencing the outlook for BoC policy as we note an elevated CAD correlation to the 2Y U.S.-Canada yield spread (0.90 on a 30 day, rolling basis). The 2Y spread has continued to widen this week, driven by a divergence in the tone of recent data (GDP, PMI’s) and thus intensifying the focus on the dual employment release at 8:30am EST (see calendar on p3). E.T. USDCAD REMAINS HIGHLY SENSITIVE TO OIL Source: Bloomberg & Scotiabank FX Strategy U.S. PAYROLLS SEEN RISING 230K; 6MO. MA AT 264 Source: Bloomberg & Scotiabank FX Strategy OIL (WTI) CONSOLIDATING ABOVE 21 DAY MA 50 day MA 21 day MA Source: Bloomberg & Scotiabank FX Strategy GLOBAL FX STRATEGY Friday, February 06, 2015 Canadian employment are expected to show a net gain of 5k jobs in January; however during 2014 the average miss on consensus estimate was 27k. Accordingly the release has tended to stray materially from consensus estimates. In the current volatile environment, CAD will be sensitive to both the Canadian and U.S. releases. C.S. USDCAD short-term technicals: neutral—momentum indicators are conflicted and the ADX highlights a softening in the bullish trend. Recent congestion has centered around the 21 day MA (1.2526) and we focus on near term support around 1.2350 with resistance expected at 1.2580 and 1.2620. E.T. EURUSD (1.1455) • EUR is weak, falling ahead of the NA session with a decline that began in response to disappointing German industrial production data and compounded by the subsequent release of Spain’s weak industrial output figures. A special meeting of euro area finance ministers has been scheduled for Feb 11, ahead of the Feb 12 leaders’ summit, with the focus of discussion expected to center on Greece. EUR’s sensitivity to headline risk remains elevated, as underscored by the Wednesday’s lifting of the ECB’s collateral waiver. E.T. EURUSD short-term technicals: neutral—technicals appear to be lacking a clear bias, and we focus on the 21 day MA (1.1494) as a near term level of resistance. A break of this level would shift the focus to the Jan 22 open at 1.1610. Near term support is expected around 1.1350. E.T. GBPUSD (1.5325) • GBP is flat, consolidating despite the release of a wider than expected trade deficit. Focus for GBP centers on the outlook for BoE policy, the next key release being the BoE inflation report scheduled for Feb 12. BoE rate expectations are neutral with a slight hawkish bias, reflecting the unanimity of the MPC as policymakers attempt to assess the medium-term implications of the recent softening of inflation. GBP has risen 1.8% this week, registering its greatest gain since February 2014 and steadily retracing its January decline. We focus on potential resistance around 1.5350 and the 50 day MA (1.5381). E.T. USDJPY (117.29) • JPY is quiet ahead of the NA session, with movement that continues to be constrained by the offsetting impact of fundamentals and a sensitivity to the broader market tone. Technicals are neutral, a reflection of the tightened range since mid-January. Short term MA’s appear to be providing resistance, and we focus on the 21 day MA (117.78). E.T. Feb 06, 2015 TECHNICALS: BUY/SELL SIGNALS AND PIVOT LEVELS 30 Day Hist Vol USDCAD 12.6 EURUSD 12.7 GBPUSD 8.7 USDCHF 61.4 USDJPY 10.1 AUDUSD 10.8 USDMXN 12.2 DXY (USD index) 7.7 EURCAD 13.3 GBPCAD 11.8 AUDCAD 11.2 CADMXN 11.2 BoC Noon Rate Spot MACD 1.2443 1.1463 1.5331 0.9198 117.25 0.7869 14.73 93.62 1.4263 1.9077 0.9792 11.84 1.2422 sell buy buy buy sell sell sell sell buy buy sell buy 9 & 21day MA buy sell buy sell sell sell buy na buy buy sell sell DMI buy sell buy sell sell sell buy buy buy buy buy sell RSI 60 43 57 46 45 39 51 57 55 67 52 39 Pivot 1st Support 1.2362 1.1345 1.5215 0.9156 116.98 0.7777 14.67 93.19 1.4186 1.8986 0.9715 11.79 Pivot 1st Resist. 1.2555 1.1540 1.5400 0.9277 117.56 0.7919 14.86 94.27 1.4340 1.9158 0.9833 11.90 Source: Scotiabank & Bloomberg 2 GLOBAL FX STRATEGY Friday, February 06, 2015 TODAY'S RELEASES & SPEAKERS Time Country Type Release (EST) 08:30 US EMPL. Change in Nonfarm Payrolls 08:30 US EMPL. Unemployment Rate 08:30 US EMPL. Underemployment Rate 08:30 US EMPL. Labor Force Participation Rate 08:30 US EMPL. Average Hourly Earnings MoM 10:30 US EMPL. Average Weekly Hours All Employees 08:30 CA EMPL. Net Change in Employment 08:30 CA EMPL. Unemployment Rate 08:30 CA DATA Building Permits MoM 12:45 US FED Fed's Lockhart (voting dove) speaks on policyl; Q&A 15:00 US DATA Consumer Credit Period Consensus Jan Jan Jan Jan Jan Jan Jan Jan Dec Dec 230K 5.6% -62.7% 0.3% 34.6 5.0K 6.7% 5.0% Last Significance 252K 5.6% 11.2% 62.7% -0.2% 34.6 -4.3K 6.6% -13.8% HIGH HIGH med med HIGH med HIGH HIGH med med-high $15.000B $14.081B low CONTACTS - GLOBAL FX STRATEGY Please contact authors directly to be added to distribution lists Camilla Sutton, CFA, CMT Chief FX Strategist, Managing Director T.416.866.5470 [email protected] Eduardo Suarez Senior FX Strategist (LATAM), Director T.416.945.4538 [email protected] Eric Theoret, CFA, CMT FX Strategist (G10), Associate Director T.416.863.7030 [email protected] Sacha Tihanyi Senior FX Strategist (ASIA ex Japan), Director T. 852.2861.4770 [email protected] IMPORTANT NOTICE and DISCLAIMER: This publication has been prepared by The Bank of Nova Scotia (Scotiabank) for informational and marketing purposes only. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness and neither the information nor the forecast shall be ta ken as a representation for which Scotiabank, its affiliates or any of their employees incur any responsibility. Neither Scotiabank nor its affiliates accept any liability whatsoever for any loss arising from any use of this information. This publication is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any of the currencies referred to herein, nor shall this publication be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The general transaction, financial, educational and market information contained herein is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. You should note that the manner in which you implement any of the strategies set out in this publication may expose you to significant risk and you should carefully consider your ability to bear such risks through consultation with your own independent financial, legal, accounting, tax and other professional advisors. Scotiabank, its affiliates and/or their respective officers, directors or employees may from time to time take positions in the currencies mentioned herein as principal or agent, and may have received remuneration as financial advisor and/or underwriter for certain of the corporations mentioned herein. Directors, officers or employees of Scotiabank and its affiliates may serve as directors of corporations referred to herein. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. This publication and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced in whole or in part, or referred to in any manner whatsoever nor may the information, opinions and conclusions containe d in it be referred to without the prior express written consent of Scotiabank. ™Trademark of The Bank of Nova Scotia. Used under license, where applicable. Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, all members of the Scotiabank group and authorized users of the mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia and Scotiabank Europe plc are authorised by the UK Prudential Regulation Authority. The Bank of Nova Scotia is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available on request. Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

© Copyright 2026 ExpyDoc