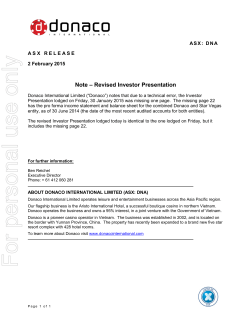

Ultimate Wealth Report A Publication of Newsmax and Moneynews Edited by Sean Hyman Vol. 3, No. 6 / June 2014 H 9 Ways to Outsmart the Average Stock Investor ave you ever been in a long line of traffic, just sitting, and think to yourself, “What is going on up there?” You keep scanning the road ahead for clues, but find nothing but parked vehicles and exasperated drivers. Finally, you inch your way forward enough to find out what’s going on — a fender bender between two cars, both pulled over to the side of the road and trading insurance information, no one hurt. Turns out it was no big deal at all, except for everyone stuck in the slow traffic that resulted. It’s human nature to stop and look at accidents, so much so that a term was coined to describe the phenomenon: “gapers delay.” In other words, a traffic jam was caused by nothing more than drivers getting unnecessarily distracted! What we all need to do instead in such situations, of course, is keep our focus on the road. If we do that, there will be a lot fewer congestion problems in major cities. Instead, everyone’s attention is on the sideshow, which makes everyone’s commute unnecessarily longer. Guess what? Investors do the same thing, in a manner of speaking. They lose sight of what’s important, with their eyes attracted to the “fender benders” along the road toward investing success. They may even take a wrong turn or a detour, or worse yet, end up in “ an accident themselves — one that may not leave them physically hurt, but sure puts a dent in their nest egg. This month, before I get to our latest stock pick (a well-positioned industry leader in a country with fantastic growth prospects), I thought it would be good for all of us to review the nine most common mistakes made by people allocating their capital in the stock market. Avoid these — which I’ve presented in no particular order — and you’ll be well on your way to a better financial future. Investors can often lose sight of what’s important, with their attention diverted toward the ‘fender benders’ along the road to investing success. 1. Watching the financial news channels for your investing advice. I freely admit, this one may sound hypocritical, since I often appear as a guest on CNBC, Fox Business, Bloomberg TV, and other outlets to give my opinions on the economy and markets. I appreciate the ability to reach so many new people, and I will continue to do so, despite what I’m about to say next. It’s not that watching financial news is bad in and of itself. It’s all about controlling your emotional reactions to what you see. The thing with news channels is that they need to fill a lot of hours of programming — and they’re competing for eyeballs, which improves advertising revenue. So, you’ll see a lot of conflicting advice ” presented to fill those hours, and you’ll see a lot of scary headlines, because that’s part of what keeps people tuning in. In addition, those channels tend to focus on very short-term advice. They watch what’s happening right now in markets, with no real view toward the longer term. They also fixate on the most popular stocks, the ones most widely held or those with a juicy, interesting story. (I call these the “cool kid” stocks, because it’s trendy or “cool” to own them, in many cases.) The problem with that is, for the most part, once a stock is popular and there’s media attention turned to it, it’s already seen the bulk of its run-up and the risk-to-reward is no longer favorable for value investors like us. If you’re making your stock selections by what you see covered on the financial news, you’re probably already too late. (Now, this outsized attention can lead to bargains too. That’s exactly what happened to Apple (AAPL). Major positive attention from the media drove the stock to all-time highs, then a brutal media backlash helped push it way back down to the undervalued state where we scooped it up. But an opportunity like that is an exception more than the norm.) So how should you use the financial news channels? I’d suggest turning to them for factual data, and not so much the opinions. In other words, what a company reports as its earnings is Sean Hyman’s extensive background in the financial markets goes back more than 20 years, including as a broker at Charles Schwab and as an instructor for Forex Capital Markets. He has held five financial licenses and has been a stockbroker, manager of a team of stockbrokers, a trading course instructor in the currency markets, a financial writer, and a key speaker at conferences both nationally and internationally. His investing philosophy is based on choosing the assets that will get “inflated” in the future — commodities — and investing in fundamentally superior currencies that will benefit from the U.S. dollar’s decline. He does it in a way that’s simple and, via the use of exchange-traded funds, can be done through a standard brokerage account. 2 fact. But an expert who says, “I rate this stock a hold,” is expressing an opinion. You can also use the financial media to gauge overall sentiment, which is one of our three prongs of analysis in Ultimate Wealth Report. When the financial media beat a drum to stay away from a sector, industry, or country for quite a while, that’s a prompt for me to start digging deeper. Are there values to be had there? On the flip side, when the media are hyping a particular stock or sector, that’s when you need to be aware. Such hype can quickly push a stock to overvalued territory (Tesla, anyone?) — and if they happen to be gaga over a stock you own, you may start to consider selling it while they’re still heaping on the sticky-sweet praise, before the backlash occurs. What that means is you want to be a contrarian thinker. If you simply go along with the crowd and do what’s popular, you’re likely overpaying for the privilege, catching stocks on the tail end of their rise. That places you in a high-risk investment with lots of downside potential. You won’t beat the market’s overall return over time doing that. For those of you subscribed to this newsletter, you don’t have to worry so much about all of this. If you follow the “buy” and “sell” recommendations I outline, and don’t get scared out of positions later by what you hear on TV, you’re avoiding the dangers. But if you are also making some stock investing decisions on your own outside of the scope of the Ultimate Wealth Report, I’d suggest you just be wary and always keep your contrarian viewpoint in order to make unbiased, emotion-free judgments. 2. Focusing on a stock price or how many shares you can buy. As I’ve explained before in Ultimate Wealth Report, a $500 stock may actually be a bargain, while a $5 stock may be completely overpriced. That’s because, when it comes to stocks, there are many interrelated and objective factors that make prices difficult to compare to one another. Stock prices are based on the underlying earnings of a company and how many total shares have been UltimateWealthReport.com June 2014 issued, among other things. When you buy a stock, you need to remember you’re buying a company, one that makes a product or service that the world needs or wants. You want to purchase companies that you believe do the best job in this regard and are in excellent financial condition. As for how much each share costs, don’t worry about that aspect. If you can only buy five or 10 shares of a great company that happens to be hundreds of dollars, that’s way better than 100 shares of a poorly-run firm with a “more affordable” $10 stock. It brings me back to the aforementioned Apple, which was $419.45 when we bought it originally. We ended up selling it at $572.29 for a 37 percent gain in a little less than six month’s time. Anyone scared off by that high initial stock price would have missed out! (Hey, even if you only had $500 and you were only able to buy one single share of Apple, your gain was still that same 37 percent.) Contrast that with CEMIG (CIG), also in our portfolio. That stock is $7.36 as of this writing, and you may have a lot of shares of it right now because of that cheap price. But so far for us, it’s only up about 5 percent including dividends. That’s not bad, but the “expensive” Apple stock did a lot better for us. Keep in mind, I’m not sour on CEMIG by any means. I still see the signs that it will give us a phenomenal return over time, and it’s worth owning. But I point it out to illustrate that stock price in and of itself is only a minor part of the story, and should not factor into your decision as to whether to buy a stock or not. It has to be taken into account with earnings, dividend yield, and a host of other considerations. “ expectations. The pros know that nine times out of 10, they are not going to catch the exact bottom in the stock when they buy, nor do they set up their expectations in their mind that way. They know that when they buy, they’ve captured value because the numbers say so (i.e., the price is low compared to a company’s earnings, financials, and prospects), but they have likely not grabbed it at the lowest possible price. The market is never perfectly predictable like that — wait too long on a stock, and you may very well miss the opportunity altogether. So instead, the most prudent course of action is to set a price target that represents a very good value, and get in when it falls to that level. (Hence, our recommended “buy” prices in our portfolios, which are determined with a lot of factors in mind.) If you instead set yourself up with unrealistic expectations to buy at the very bottom of a stock’s drop and sell it at the very tippy top of a run-up, you’ll usually end up extremely frustrated. You’ll also tend to make rash decisions on both ends of the spectrum that cost you. Consider the actions of guys like Warren Buffett, Sir John Templeton, and Peter Lynch, among others. They never got discouraged if they bought a stock that fell further in the near term. They knew better — they had done their homework, and fully understood the true value of what they were holding. They also don’t beat themselves up for selling a stock that continued to rise afterward. Their goal was to make money, and overwhelmingly, they did so with patience, and most importantly, without having to call the exact bottom and top. They bought into a position, waited for the market to catch up to them, and then sold when they had an appreciable profit. From the value investor’s perspective, the biggest factor in your overall gain comes more from the buy price — assessing and capturing value while the stock was priced cheap relative to Anyone scared off by Apple’s $419 share price would have missed out on a 37 percent gain in a little less than six months. 3. Expecting to “call the bottom” when you buy or “call the top” when you sell. One of the biggest differences between a professional investor and the novice are their June 2014 Moneynews.com ” 3 its earnings and net assets. Get the buy right and the sell isn’t so hard. Picking up stocks at a lower point of valuation than the average investor means you have a great shot at ending up with a much better overall return — with less risk to boot, since you paid less on the front end for a stock’s earnings and assets. 4. Focusing too much on the level of the Dow Jones Industrial average or S&P 500 Index and not enough on the valuation at which you bought your individual stocks. Think Buffett sweats the Dow every day? Not a chance. Buffett and others of his breed are not buying the overall market, they’re buying companies. The only price that matters to them is the price they are paying for those companies, no matter what the Dow or S&P as a whole may be doing. Certainly, overall market corrections may take a great stock down with it temporarily, but that isn’t a reason to panic — if you’ve chosen wisely, that’s a chance to buy more of it. Investors like Buffett use corrections to their advantage, but only if they focus on the valuation of the company and what it’s really worth. The key is to seek out undervalued industries, sectors and/or countries, and then identify the best undervalued stocks within them. Even in an overvalued market, there will almost always be a few pockets of value. You just have to be pickier in scrutinizing companies when the overall market is overvalued. It gets easier in a huge sell-off, where many areas of value appear . . . except that, in such situations, many people let fear scare them away from making a move. (Remember my advice: Be a contrarian.) 5. Using stop-loss orders. Short-term traders — those holding a stock for minutes, hours, days, or just a matter of weeks — may benefit from the use of stop-loss orders, which trigger a “sell” if a stock hits a predetermined price. But at least in my opinion, the true investor doesn’t really need them to manage his or her risks. If anything, automatic triggers to sell a stock can become the enemy of the true investor as the 4 market whipsaws on a very short-term basis and thus unnecessarily stops them out. When that happens, you may have simply locked in losses on a company that may still be way undervalued and set to eventually climb — it forces you out too soon, before the trade can run its due course. So, if you don’t use stop-loss orders, how can you manage risk? Well, by knowing what you’ve purchased. You want to know the answers to such questions as: • Is it a sizable company with significant market share? • Does it have lots of cash on its books and low debt levels? • How are its profit margins? • Are the price-to-earnings and price-to-book ratios low enough to represent a good value? These are among the questions I ask for each investment that I consider, in order to assess the risks in owning a particular stock. We also manage risk through targeted diversification. In time, if you’ve built up a portfolio of anywhere from 10 to 30 stocks that are huge companies with billions of dollars of cash on the books, with low debt levels relative to their size and P/E and P/B ratios that are historically cheap, then you have managed your risks very well, I’d say. This is how the true investor manages risk, not with stop-losses that generally do nothing more than lock in losses and generate unnecessary commissions for your broker. 6. Chasing the “popular” stocks. Facebook. Twitter. LinkedIn. Chipotle. Amazon. Netflix. Priceline. These stocks have been market darlings at some point, leading to a surge in their popularity that was, at times, well beyond the fundamental numbers. People are buying such stocks on nothing more than hope, in part fueled by the positive noise from financial news outlets. Are they bad companies, per se? Not necessarily — but no matter how good a company may be, there’s definitely such a thing as paying too high a price. It’s like paying $1 million for a beautiful $300,000 home. Sure, it’s a nice house, but you’ve UltimateWealthReport.com June 2014 spent too much for it, excessively so, and it may be years, if ever, that you see it reach the value you’ve paid. (Twitter investors recently learned this hard lesson, as the stock shed nearly half of its value this spring.) Novice investors crave the emotional comfort of being in stocks that others are in too. They also love the fact that the companies usually seem to deal in something exciting, cutting edge, and new. The problem with new things is that most of the stocks won’t survive even though the technology does. Sometimes, it’s better just to buy the product or use the service but not buy the stock. For instance, I’ll use Facebook, Twitter, and LinkedIn and get the benefits of what they have to offer. But making an investment in them would be a dire mistake. These stocks will routinely be overvalued and are in industries that are very unpredictable. Think about how quickly a social media stock becomes a “has been” as a new competitor takes its place. (The cautionary tale of MySpace forever stands as an example of what can happen to this type of website, and how quickly the whole success story can collapse.) Is that the sort of gamble you want to take with your money? I know I don’t want to take those kinds of risks with my money, so I’m certainly not going to suggest you doing it with yours in this newsletter. “ value even after huge declines. Investing in IPOs is only suitable for wellestablished savvy investors with a high net worth. The people in those lofty tax brackets are in a much better position to obtain such stock at a better price, and they can take bigger risks. They’ll invest in not just one IPO, but 10 or more, knowing that seven or eight might not pan out, but the two or three that do will make it worth their while. The average investor should not take such risks, since losses can affect their lifestyles and delay their retirement date in worst-case scenarios. You need your investments to win seven to eight times out of 10, and not settle for the long-shot risks inherent in an IPO. I don’t care if you’ve got $10,000 or $1 million in investable assets — my advice would be the same. Stay away from IPOs. They’re appropriate only for those who understand the huge risks and have a net worth in the tens of millions of dollars at least. They may sound exciting, but IPOs are nothing more than a trap, especially for individual investors. 7. Investing in initial public offerings (IPOs). They may sound exciting, but IPOs are nothing more than a trap, especially for individual investors. For starters, many IPOs won’t even be in existence a few years from now. That’s just a reality of the business environment. Second, many of them will depreciate 30 to 60 percent from the price at which they go public over the following three to nine months. Thirdly, they’re typically so overpriced from the very beginning that they’re still usually not a great June 2014 ” 8. Having too short of a time horizon. Hey, who wouldn’t want to earn 30 percent in 30 days rather than 12 or 18 months? But for the most part, it just doesn’t work that way. Still, novice investors start off with a get-richquick mentality. You may wonder why you can’t be successful chasing quick returns. You have to remember, in purchasing a stock, you’re getting the company behind it. Those businesses make products or deliver services, and the stock can sustain a higher stock price only because the company is truly worth more. What makes it worth more? Part of it is due to the assets it owns, but most of the worth comes from the earnings it produces. The more money it earns annually, the more the company is justifiably worth. Increasing that takes time. You don’t double profits overnight; it’s a slow and steady climb that ultimately wins the race. Moneynews.com 5 Same goes for investing in that company. You purchase it in an undervalued state, then hold on as (a) the market catches up to what you’re seeing valuation-wise, and (b) the company builds its sales and earnings to justify an even higher stock price. There are no reliable shortcuts. If you’re impatient, you’ll never make it as a good investor. Not only will you rack up trading costs by excessively buying and selling, you’ll never give your investments the proper time to grow. You’ll find that it’s easier to make $1,000 by buying once and selling once than it is to make, say, 10 trades and capture $100 each time. You’ll find that you have 10 times the costs to overcome than in the first scenario, so you’d need to be that much better than the investor who just bought a good company and was patient. It doesn’t mean your investing system is broken — it actually indicates it’s working, if your winners are, in sum, outpacing your losers over time. Putting Our Knowledge to Work I’d like to point out that most of the mistakes I’ve covered in this issue revolve around thinking. The astute investor maintains a certain mindset that those who lose money over time do not. The Ultimate Wealth Report keeps you in the former camp. In the weekly updates, I let you know the fundamental and technical state of our holdings, so you can avoid negative reactions that cause bad decision-making in buying or selling. For a low annual price, I’m offering an education in real-life investing, with coaching each week and this monthly newsletter. My hope is that my subscribers can use this to set a prosperous future for this and coming generations of their own families. This month, we have our latest opportunity to grow our nest eggs. Putting to action my advice about finding value, we are venturing beyond the U.S. borders — since U.S. markets are still overvalued in technical terms as of this writing — Chart 1 9. Thinking that every investment must pan out. Even with the best system and best analysis, there are going to be times when an investment or two won’t return a profit, and should be sold at a loss. No one has a 100 percent winning track record — and if they do, they’ve probably passed up too many opportunities along the way out of CNOOC Limited (CEO) Weekly Price, 2007-2014 over-caution, and dinged their overall 90 RSI potential return in the process. 50 As I pointed out earlier, diversification 10 is the key in this regard. Say you have a $240 Stock Price portfolio of 20 stocks and you’ve spread 220 your money evenly between each of 200 them. You’ve got five percent of your 180 160 money in each stock. If one or two of them 140 were to drop, you can recover from that. 120 But if you own one company and it falls, 100 200-Week Moving you’re in trouble. 80 Average 60 Remember, I scrutinize each potential 7M Volume investment very thoroughly. The chance 5M of even one of our companies going 3M 1M completely under is highly unlikely Jul ’07 Jul ’08 Jul ’09 Jul ’10 Jul ’11 Jul ’12 Jul ’13 Jul ’14 because they’re so cash rich. This eight-year price chart of CNOOC reveals the upward-sloping 200But no matter if you’re investing along week moving average and the current range-bound state of the stock. with my recommendations in the Ultimate These sideways ranges tend to break out strongly, and I think in this Wealth Report or finding stocks on your case to the upside based on a number of bullish fundamental factors. own, set your expectations: If one or two SOURCE: StockCharts.com stocks out of 15 or 20 falters, you’ll be okay. 6 UltimateWealthReport.com June 2014 Chart 2 and exploring a part of the world where CNOOC Limited Stock Price, One Year there’s still value to be found: Asia. RSI 90 Asian stocks as a whole are cheap, in 50 part fueled by the fact that the United 10 States has been on a bull run for the $210 Stock Price 200-Day Moving last few years, grabbing the attention of Average 200 the investing public. China especially is 190 suffering from an overly pessimistic view of 180 its economy, and that’s pulling down many other countries in that nation’s orbit. 170 50-Day Moving The pessimists have been out in force, 160 Average overreacting to reports that China’s 150 economy slowed from 7.8 percent to 7.4 Volume 500K percent annual GDP growth. You’d think it 300K had dropped to 4 percent based on investor 100K reaction. They’ve overplayed it, leaving a May Jun Jul Aug Sep Oct Nov Dec 2014 Feb Mar Apr May number of incredible values in the wake. CNOOC stock suffered a sharp decline from a September 2013 high Thanks to the emotional, mostly to a March 2014 low. But the stock has since found some footing, irrational overreaction, Chinese stocks have climbing above its 50-day moving average. The Relative Strength fallen. Last month, we jumped on board Index (RSI, represented at the top of the chart) continues to gain this phenomenon, taking advantage by steam as well. buying China Mobile (CHL). SOURCE: StockCharts.com And this month, I’ve pinpointed another strong stock for our Global Value an operating margin of 26.78 percent. In addition, Portfolio: CNOOC Limited (CEO), a subsidiary of we know that the management team is doing a China National Offshore Oil Corporation. good job of running the company and allocating CNOOC explores for, develops, produces and its capital by its return on equity (ROE) of 17.34 sells crude oil, natural gas, and other petroleum percent, outpacing the benchmark of 15 that products. It produces offshore crude oil and natural Buffett looks for. gas primarily in Bohai, the Western South China This company made $21 billion last year in Sea, Eastern South China Sea, and East China Sea. earnings (EBITDA) and has $14.62 billion in cash It owns oil and gas assets in Asia, Africa, North on its books, which helps support a solid dividend America, South America, Oceania, and Europe. of 4.5 percent. There’s a lot to love with this huge $73 billion On the other side of the ledger, CNOOC’s company right now. It has a trailing and forward debt levels are low and manageable. The debt P/E of 8 — so it trades at eight times its earnings, is $21 billion, which isn’t too much for a $73 versus the S&P 500 Index average of 18 times. billion company. (Debt levels need to be below 50 The price-to-book ratio is 1.36, meaning it percent in my opinion, but ideally no more than trades at a great price relative to its net assets. (P/B 33 percent of the worth of the company. CNOOC ratio is the stock price divided by the company’s comes in at just under 29 percent.) book value per share from the most recent quarter All in all, the fundamentals are screaming “buy.” of data). In fact, just its assets alone (not counting I think we should listen, knowing CNOOC is any of its earnings) are worth $122 per share, priced right relative to its earnings and net assets. which is impressive considering its current stock Of course, before making such a decision, I also price around $160. always make sure the technical indicators line up. Margins are another area where CNOOC (For those of you who are new to Ultimate Wealth shines, with a profit margin of 19.75 percent and Report, those are all the various tools I use to June 2014 Moneynews.com 7 pick at a glance CNOOC LIMITED (CEO) price: $163.33 (as of May 7, 2014) 52-week range: $147.24-$211.49 market cap: $73 billion p/e ratio: 8 dividend yield: 4.50% profile: CNOOC Limited is an investment holding company in the business of exploring, developing, producing, and selling crude oil, natural gas, and other petroleum products. CNOOC produces offshore crude oil and natural gas primarily in Bohai, the Western South China Sea, the Eastern South China Sea, and East China Sea in offshore China. In addition, the company owns oil and gas assets in Asia, Africa, North America, South America, Oceania, and Europe. analyze the stock price movements over the short-, medium- and long-term. So what do those technical indicators say? I’ll start with an eight-year chart showing the weekly prices, which smooths out daily fluctuations and gives a nice longer-term picture. (See Chart 1 on Page 6.) First of all, notice that the overall trend is upward, as shown by the 200-week moving average. Yet, there has been a sideways consolidation of the price for about two and a half years and counting. If you’ve been a reader for a while, you know — these sideways ranges can explosively break out into long, strong trends. The key is to pick up these types of stocks toward the latter part of their range-bound trading period, as near to the range’s low as you can get. Generally, ranges going on for two to three years are near their end. On the chart, you can see the sideways range low tends to hold in the $145 to $150 area. But with the trend up overall, and the P/E so low at this point, I think now represents a good time to jump into this stock. From here, if the stock only goes up to the top of its range, it would still be a 33 percent increase from the current price. Not only do I foresee that as likely, I think it’s capable of returning to its all-time highs of $240 per share. (Remember, its forward P/E is only 8, so it has a lot of room to run before we could consider it overvalued.) 8 Delving into the realm of Elliott Wave for a moment, going all the way back to where the stock first started trading in 2001 shows the stock price is currently in a wave 4, meaning we should see a wave 5 advance higher in the months to come. You may not be overly familiar with Elliott Wave — and you don’t have to be to understand and follow Ultimate Wealth Report — but just know that wave 5’s typically at least reach the level of the wave 3 peak, which in the case of CNOOC Limited was $240 per share; often they’ll even exceed that peak. Based on my past success with Elliott Wave, that pattern gives me great confidence in the potential for CNOOC’s rise going forward. To get an even better idea as to why I think it’s smart to buy CNOOC right now as opposed to waiting any longer, we can swoop in for a closer look at the price patterns with the daily-price oneyear chart (See Chart 2 on Page 7), which reflects daily closing prices versus the weekly prices. From September 2013 to March 2014, we can see that CEO shed nearly 30 percent of its stock price. We can also see that investors finally panicked and threw in the towel en masse back in January of this year, based on the spike in trading volume (bottom bar chart). Then in February, the downtrend line was broken, which indicates the “smart money” (large institutions) were likely returning. Sure enough, the stock bottomed in March and climbed back above its 50-day moving average in April. Now that moving average has turned up and the Relative Strength Index continues to trend higher, it seems the bottom has been set already. Even if it hasn’t, however, the technical indicators show the bottom is likely near. The two most likely scenarios in my view are either a drop followed by a spike higher, or simply a push mostly higher from here. I expect that this stock could hit its former 52-week high around $210 per share and even its all-time high above $240 within the upcoming 12 to 18 months. Thus, my recommendation is to buy CNOOC Limited (CEO) at or under $180 per share for the Global Value Portfolio. UltimateWealthReport.com June 2014 Best Buys of the Month This new “Best Buy” section will be an ongoing addition to the newsletter. I have decided to add it based on some of the feedback I’ve received from our subscribers, many of whom are new to the service and wondering, “What should I buy first?” After all, I realize most of us have limited capital, and the thought of buying a ton of stocks at once can be daunting. These stocks are my favorite picks to buy right now, and represent what’s best among all of our holdings as far as pricing versus value at the time we go to press. So, if you’re new to the Ultimate Wealth Report, or you have recently amassed some new investing capital to deploy, I’d suggest you start with the following three picks first, along with this month’s new addition, CNOOC (CEO). “ and wait for a pullback. I’m not saying it’s not a good stock above $48, but I choose my buy-in prices based on optimizing the value as best we can. Be patient and let the price come back to you at or under $48. If you do purchase China Mobile, definitely take the time to go back to the May 2014 issue and re-read the original write-up. You’ll see all the reasons to hang on, even if the stock happens to gyrate over the coming months. China Mobile may indeed ride up and down with any tumult in the Chinese market at large, but in the end, its fundamentals will carry the day. And if it doesn’t fall below $48, allowing you to buy in? Don’t worry . . . a key for this or any of my recommendations is to adhere to my suggested buy at or under prices. Don’t chase a stock that’s out of reach. Instead, just turn to the others in our list that are in my range. It’s better to stay disciplined in your quest for a market-beating return, and never overpay. Last month, I recommended China Mobile at or under $48, and I’m just as excited about its prospects now. JUNE BEST BUYS Price* 52-Week Range Yield China Mobile (CHL) Security $47.31 $41.35-$57.42 4.77% iShares FTSE China 25 Index Fund (FXI) $34.61 $31.35-$40.32 2.93% Petrobras (PBR) $15.66 $10.20-$19.17 N/A * As of May 7, 2014 China Mobile (CHL) In last month’s issue, I recommended China Mobile at or under $48 per share, and I’m just as excited about its prospects now as I was then. This $183 billion company, with $38.06 billion in earnings (EBITDA) last year, a profit margin of around 20 percent, and a return on equity of more than 16 percent, is solid fundamentally, with bright growth prospects to come in a technologically hungry Chinese marketplace. In addition, China Mobile is cheap, with a P/E just under 10 and a P/B of 1.42. For that, you’re getting an enormous, dominant company in a growing industry that pays a dividend of over 4 percent. I want to add, be aware that when you get this newsletter in hand, the stock may have popped above $48. If so, don’t buy it — put it on your radar June 2014 ” iShares FTSE China 25 Index Fund (FXI) I realize I have talked extensively about China in these past two issues. But there’s a reason. China, as far as investors are concerned, is a hated country right now. Sentiment on its economic prospects is lousy. Sounds bad, right? Not if you’re a value investor. It’s at these points where value investors should get very interested and start poking around. That’s where the iShares FTSE China 25 Index Fund (FXI) comes into focus, as a way to play the broader Chinese market at a low entry price. This ETF has a P/E of 7, while the S&P 500 has a P/E of 18. Investors are overpaying for the S&P 500 right now and most don’t realize it. Meanwhile, they despise what’s undervalued, which is China. If you ever wondered why the masses can’t beat the market, there’s why. It’s flawed investor psychology at work. Consider FXI at or below $44 per share. Moneynews.com 9 Petrobras (PBR) Brazil has been another market that has been hammered with bad sentiment. Investors are still shying away from Brazil and they shouldn’t — but that’s typical, judging on what has been instead of looking forward. Brazilian stocks took a licking for the last three years. But the valuations are compelling at this point, and it’s one of the few pockets of value available in the world right now. Recall that I said an industry, sector, or country that has been beaten down for two to three years warrants a close look. The P/E ratios and Elliott Wave counts on long-term weekly price charts can tell that tale. In short, if the P/E’s are 10 or under and the Elliott Wave counts are a wave C through a wave 2, then it’s worthy of investment. Drilling down from there, you can look at the fundamentals of individual companies that may warrant investment, choosing among large, wellcapitalized companies. That brings us to Petrobras, a $90 billion oil company with a trailing P/E in the 7s and a forward P/E in the 6s. It trades under its book value with a price-to-book ratio of 0.54, which puts the book value per share at $26.20. As I’m writing this, PBR is trading around $15, meaning you can get the stock for less than the value of its total assets! Petrobras generated $32 billion in earnings (EBITDA) last year and has almost $23 billion in cash on its books. Additionally, we can look at what the large institutional investors are doing to find that a lot of buying took place in March, when the stock was in the $11 to $12 range. The big players see a lot of value there. On top of that, the Brazilian stock market as a whole is about to end a wave 2 and PBR is ending its wave C correction. These are points of maximum pessimism, which represent the times of greatest opportunity. I recommend Petrobras at or under $16, bumping that up from $15 previously. “ Market Update: Commodities Surging Something is happening that isn’t getting its fair share of attention in the financial media: The CRB Commodity Index, a basket of 19 widely used commodities, hit a fresh 52-week high, while the U.S. dollar index sunk to a new 52-week low. Oh, the media was all over the story when commodities were struggling and the dollar was bouncing higher. Experts were calling the “end of the commodity super cycle” and throwing around the term “king dollar” for two and a half years. But now that the realities have changed, those same experts have gone silent. Huge technical milestones have been overcome in the commodities market. A threeyear downtrend has been solidly broken to the upside. The CRB Index has climbed above its 50-week moving average and its 200-week moving average, in addition to setting that 52-week high. Additionally, the U.S. dollar is not just setting a new 52-week low, it’ll soon be at a two-year low. It may see a bounce higher near-term, but overall the trend in the buck has been downward since it reached a top last summer. Why aren’t they talking about it? Well, market cheerleaders realize it’s not good when inflation is rising and the dollar is falling. The politicians in D.C. know that, and they’ve worked hard to convince us that there is no inflation happening. If you tell people something for long enough, they tend to take it as fact, whether it’s true or not. But thankfully, charts don’t lie — throughout 2014, commodities have been on a tear! At least Ultimate Wealth readers are aware of it. And better yet, our portfolio is poised to benefit from inflation’s rise and this dollar devaluation. Our stocks with a global reach will earn tons of money in foreign currencies, which will be good with the U.S. dollar ailing. The remainder of our portfolio benefits from the rise in the cost of living — as oil, gasoline, natural gas, steel, and coal go up in price, so do the profits of the companies that we own. Brazil’s stock market valuations are compelling after three difficult years; it’s one of the few pockets of value in the world. 10 UltimateWealthReport.com ” June 2014 CORE VALUE PORTFOLIO RECOMMENDATION Entry Date Symbol Devon Energy DVN Entry Price Recent Price Buy at or Under Current Yield Effective Yield Total Return† 27-Sep-12 $59.31 $73.06 $62.00 1.20% 1.48% 25.88% Peabody Energy BTU 7-Nov-12 $26.00 $18.41 $26.00 1.85% 1.31% -21.03% PowerShares Agriculture DBA 19-Apr-13 $25.94 $29.03 $30.00 N/A N/A 11.91% Newmont Mining NEM 21-May-13 $31.74 $24.01 $38.00 3.33% 2.52% -21.84% iShares Silver Trust SLV 22-Jul-13 $19.60 $18.57 $21.00 N/A N/A -5.26% HollyFrontier HFC 23-Oct-13 $45.39 $51.91 $47.00 6.16% 7.05% 17.04% Apple AAPL 26-Feb-14 $518.15 $592.33 $520.00 2.06% 2.35% 14.31% GLOBAL VALUE PORTFOLIO RECOMMENDATION Entry Date Symbol Entry Price Recent Price Buy at or Under Current Yield Effective Yield Total Return† Petrobras PBR 30-May-12 $19.12 $15.66 $16.00 N/A N/A -15.45% Vale S.A. VALE 27-Sep-12 $18.22 $13.55 $22.00 6.45% 4.80% -16.55% Teck Resources TCK 24-Oct-12 $31.34 $22.31 $33.00 3.89% 2.77% -25.12% Barrick Gold ABX 27-Nov-12 $35.13 $17.28 $43.00 1.16% 0.57% -49.33% Companhia Energetica CIG 27-Nov-12 $8.47 $7.36 $12.00 7.84% 6.81% 5.66% EPI 27-Nov-12 $18.00 $19.13 $21.00 1.20% 1.28% 7.38% DCM 20-Dec-12 $14.56 $15.96 $16.50 3.63% 3.98% 13.98% WisdomTree India Earnings NTT DOCOMO iShares FTSE China 25 FXI 24-Jan-13 $41.57 $34.61 $44.00 2.93% 2.44% -14.34% Market Vectors Russia ETF RSX 26-Feb-13 $28.86 $23.90 $35.00 3.05% 2.53% -17.19% Agrium AGU 25-Nov-13 $89.01 $94.63 $92.00 3.17% 3.37% 8.03% iShares MSCI Turkey TUR 18-Dec-13 $52.40 $54.90 $62.50 2.03% 2.13% 4.77% China Mobile CHL 23-Apr-14 $45.03 5.02% 5.06% $47.31 $48.00 4.77% COPEL# ELP $15.33 $12.60 2.90% CNOOC Limited# CEO $163.33 $180.00 4.50% BUY BUY SOLD POSITIONS RECOMMENDATION Symbol Entry Date Entry Price Exit Date Exit Price Total Return† YPF YPF 21-May-13 $13.84 12-Sep-13 $18.18 32.52% iShares MSCI Italy Index EWI 24-Jul-12 $9.33 12-Sep-13 $13.78 51.46% iPath DJ-UBS Cocoa NIB 24-Aug-12 $32.55 16-Oct-13 $36.69 12.72% Apple AAPL 20-Jun-13 $419.45 5-Dec-13 $572.29 37.58% Corning GLW 20-Mar-13 $12.90 5-Dec-13 $16.73 32.26% ArcelorMittal MT 26-Jun-12 $14.26 30-Dec-13 $17.72 27.74% Total SA TOT 20-Dec-12 $51.90 30-Dec-13 $61.04 22.72% BP BP 24-Jan-13 $44.14 2-Jan-14 $47.96 12.92% Freeport-McMoRan Copper & Gold FCX 26-Feb-13 $31.87 2-Jan-14 $37.65 28.99% Encana ECA 20-Apr-12 $18.39 2-Apr-14 $21.42 25.07% Royal Dutch Shell plc RDS-B 29-Jan-14 $73.00 30-Apr-14 $84.67 17.34% # Recommendation not bought yet. All as of close May 7, 2014 † Notes on all portfolios: “The “Total Return” column includes all reinvested dividends at concurrent recommended buy prices. Returns calculated based on a purchase of $1,000 of the security on the listed entry date and price. The “Effective Yield” column reflects the yield investors receive assuming they bought at the entry price and followed all subsequent recommendations. June 2014 Moneynews.com 11 Ultimate Wealth Report Ultimate Wealth Report is a monthly publication of Newsmax Media, Inc., and Newsmax.com. It is published at a charge of $109 for print delivery ($97.95 for digital/online version) per year through Newsmax.com and Moneynews.com. The owner, publisher, and editor are not responsible for errors and omissions. Rights to reproduction and distribution of this newsletter are reserved. Any unauthorized reproduction or distribution of information contained herein, including storage in retrieval systems or posting on the Internet, is expressly forbidden without the consent of Newsmax Media, Inc. For rights and permissions, contact the publisher at P.O. Box 20989, West Palm Beach, Florida 33416. To contact Ultimate Wealth Report, to change email, subscription terms, or any other customer service related issue, email: [email protected], or call us at (888) 766-7542. © 2014 Newsmax Media, Inc. All rights reserved. Newsmax and Moneynews are registered trademarks of Newsmax Media, Inc. Ultimate Wealth Report is a trademark of Newsmax Media, Inc. Financial Publisher AARON DeHOOG Editorial Director/Financial Newsletters JEFF YASTINE Senior Financial Editor SEAN HYMAN Art/Production Director PHIL ARON DISCLAIMER: This publication is intended solely for informational purposes and as a source of data and other information for you to evaluate in making investment decisions. We suggest that you consult with your financial adviser or other financial professional before making any investment. The information in this publication is not to be construed, under any circumstances, by implication or otherwise, as an offer to sell or a solicitation to buy, sell, or trade in any commodities, securities, or other financial instruments discussed. Information is obtained from public sources believed to be reliable, but is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted. In no event should the content of this letter be construed as an express or implied promise, guarantee or implication by or from Ultimate Wealth Report, or any of its officers, directors, employees, affiliates, or other agents that you will profit or that losses can or will be limited in any manner whatsoever. Some recommended trades may (and probably will) involve commodities, securities, or other instruments held by our officers, affiliates, editors, writers, or employees, and investment decisions by such persons may be inconsistent with or even contradictory to the discussion or recommendation in Ultimate Wealth Report. Past results are no indication of future performance. All investments are subject to risk, including the possibility of the complete loss of any money invested. You should consider such risks prior to making any investment decisions. See our Disclaimer, as well as a list of stocks that the Senior Financial Editor owns by going to UltimateWealthReport.com. 12 Closing Thoughts Investing in stocks is not easy. It’s not because it’s hard to open a brokerage account and make trades — these days, it’s actually fairly simple for nearly anyone to access the stock market, which wasn’t the case at all years ago. The problem is this: We’re all human. That’s a wonderful gift, of course, but it also brings with it the imperfections of the human brain and how it operates. It’s difficult to think clearly and logically, and make decisions without an emotional component. When the stock market drops, those with investments worry. When your own particular investments drop, you might tend to panic. It’s been proven that the fear of losing money is stronger than the hope of gaining it, and thus people tend to “cut their losses” too soon. The pull of crowds, and opinions of people you see on TV, also tends to emotionally sway people to make knee-jerk decisions. There are a million ways to go wrong when you invest. You need the courage of your convictions, knowing that you are doing the right thing even when other investors are thundering toward the exits. You can’t wilt under popular opinion, buying stocks when they are all the rage and selling whenever yours has a setback. You’ll buy too high and sell too low, increasing your risk along the way. In this issue, I outlined nine common mistakes investors make. They’re themes I’ll return to, as I lead you through any tough times to the profits one can reap from long-term investing. That’s my mission, one I take very seriously with each recommendation I make. Actions to Take Now Action No. 1: Buy CNOOC Limited (CEO) at or under $180 per share for the Global Value Portfolio. Action No. 2: If you’re new to Ultimate Wealth Report and are wondering which stocks may be best to start your portfolio with, consider China Mobile (CHL) at or under $48, the iShares FTSE China 25 Index Fund (FXI) at or under $44, and Petrobras (PBR) at or under $16. Those represent especially good bargains in our portfolio right now. Also, note on the Page 11 portfolio chart that I’ve also slightly bumped up our target “buy” price on COPEL (ELP) to $12.60 from $12.00. God bless! Sean Hyman To subscribe to this newsletter, please go to www.moneynews.com/offer UltimateWealthReport.com June 2014 Why Just Wear an Ordinary Watch . . . When You Can Wear a Heart Rate Monitor That Also Tells Time? Especially When You Can Grab This Heart-Healthy ‘Smart Watch’ At a Hefty 84% Discount! Yours for only $7.95 (plus s&h) A s a savvy Newsmax reader, you’ve been selected to receive a very special offer with our compliments. We’ve reserved a Heart Rate Monitor “Smart Watch” (a $49.95 value) at a hefty discount for you, while supplies last. This is just our way of showing you our dedication to your health. You may wonder why we care . . . Well, every 38 seconds, another American dies from heart disease. During the course of a single day, that adds up to a whopping 2,300 deaths. So it’s easy to see how heart ailments kill off more American men and women than any other condition. And as the publisher of the popular Health Radar, Newsmax takes its commitment to your health seriously. So when we got a great deal on a shipment of these Heart Rate Monitor Watches, we unanimously decided to pass on a hefty discount to you, too — because every tool you have in your own health arsenal helps lower the odds you will become one of these sad statistics. Now, you know you need a watch anyway . . . So Wear a Watch That Could Help Save Your Life An average normal heart beats from 60 to 100 times a minute at rest. Do you know what your heart does at rest — and during exercise? If you want to ensure your optimal health, you really should. Finally, monitoring your heart rate is as simple as wearing a watch! Without the use of a chest strap or feeling uncomfortably attached to any wires, this unique watch allows you to check your own heart rate and calculate calories burned — with just a . . . [ CONTINUE TO NEXT PAGE FOR MORE INFORMATION ] Continued from previous page slight touch of your finger. Whether you’re walking, playing golf or tennis, or just relaxing, your Heart Rate Monitor Watch makes it easy for you to know what your heart is doing. Plus — now you can make sure you’re not overdoing it. It looks like a sports watch (so no one will suspect you’re monitoring your long-term health) . . . And despite the high-tech benefits, this watch is as simple to use as 1-2-3. Because of the deadly consequences of heart disease, Newsmax decided to send you the Heart Rate Monitor “Smart Watch” for only $7.95 (plus shipping & handling) — a full 84 percent off of the normal price of $49.95! Plus, to ensure that you receive critical health information, we at Newsmax also agree to include a three-month trial subscription to its popular Health Radar. In your three-month trial subscription to Health Radar, you’ll get the latest studies, updates, and medical advances from the worlds of both conventional and alternative medicine. First, along with setting time and date, you enter your age, weight, and gender. This information is stored in the watch’s memory. Second, when you begin exercising, you simply start the watch’s internal counter. Plus, you’ll also find easy-to-read strategies to help you fight heart disease, weight gain, dementia, diabetes, cancer, stroke, depression, and many other conditions that prevent you and your loved ones from living an active, funfilled life. And third — when you finish, you simply stop the counter, press SET, and touch the sensor once lightly. Based on your preset information, the time on the counter, and your heart rate, your watch will tell you how many calories you burned during your workout. It’s that easy . . . And of course, you’ll receive a complete instruction manual with the watch. Plus, additional features of your Heart Rate Monitor Watch include: ■■ Easy-to-read time and date ■■ Daily alarm and hourly chime It’s time to move beyond the limits of old-fashioned medicine. And move beyond those nagging health problems that make you feel tired, sick, fat, weak, and stressed out. No matter what health issues you may be coping with, you’ll discover every issue of Health Radar to be an outstanding source of useful action strategies that help you enjoy the life you were supposed to live! ■■ LCD screen display ■■ Chronograph (stop watch) with split-lap time ■■ Pulse mode to check your pulse at any time ■■ Backlight to see the dial in the dark ■■ Stainless-steel back ■■ Battery included 3 MONTH TRIAL with this offer! Get the Heart Rate Monitor “Smart Watch” for only $7.95 — a $49.95 value! You’ll pay the standard $4.95 shipping and handling fee. Plus, you’ll also receive a three-month trial subscription to Health Radar! ORDER NOW: Get Your Deeply Discounted Heart Rate Monitor Watch Today! www.Newsmax.com/HeartWatch See Website for terms, conditions and eligibility for this offer.

© Copyright 2026 ExpyDoc